Dollar Rally is Fools’ Gold and Should be Sold, Analyst Says

- Written by: Gary Howes

- USD sold with CAD, NZD & AUD bought at CBA.

- As April CPI gets USD’s bulls hot under the collar.

- Creates buying opportunities in other currencies.

- ”Transitory” CPI may already have seen its peak.

Image © Adobe Images

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

The U.S. Dollar rebound should be sold into over the coming days, according to analysts at Commonwealth Bank of Australia, who’re advocating that investors take advantage of the resulting buying opportunities in commodity currencies while insight from Capital Economics suggests that U.S. inflation may already have peaked.

Dollars were bought in exchange for all but a handful of currencies from the mid-week session after the Bureau of Labor Statistics said U.S. inflation had reached its highest level since September 2008 during April, while the greenback’s rally gathered pace on Thursday as stock markets fell heavily across the globe.

U.S. inflation rose by 4.2% during the 12 months to April, up from 2.6% previously and more than twice the 2% target of the Federal Reserve (Fed), while even after excluding volatile food and energy items from the basket of goods and services measured the annualised rate of price growth still came in at 3%.

Core inflation, which is typically seen as a more meaningful gauge of prices because it ignores changes in commoditised food and energy items, was up from 1.6% in March and may have led some in the market to assume that such increases could see the Fed abandon its new inflation targeting strategy in favour of interest rate rises that come far sooner than the bank has so-far guided for.

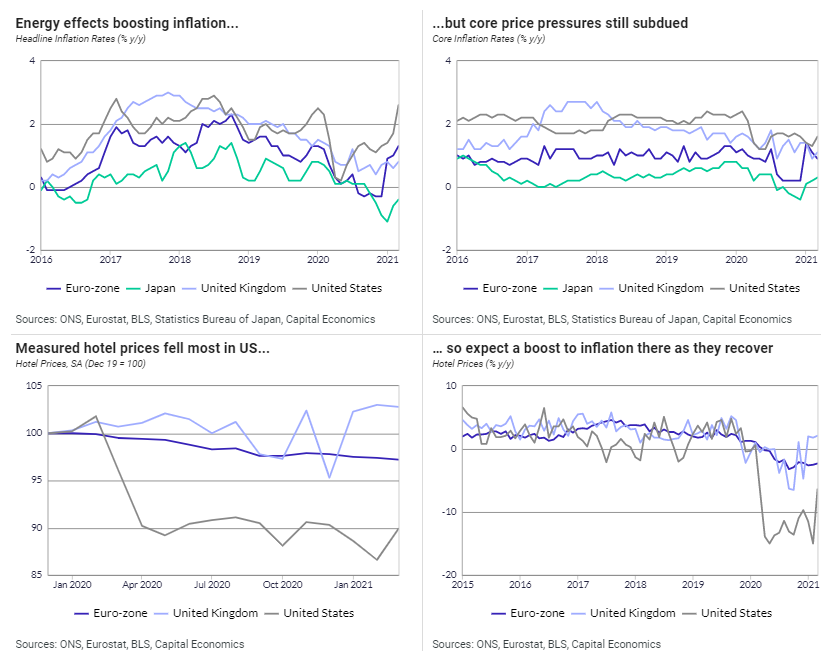

“There will be a mechanical rise in inflation in both the US and Japan on the anniversary of previous falls. Both effects are temporary and shouldn’t be confused with evidence that underlying inflationary pressure is stronger than that in Europe,” says Gabriella Dickens at Capital Economics.

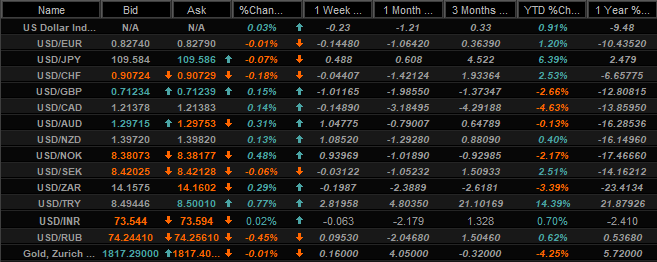

Above: U.S. Dollar exchange rate quotes and performances. Source: Netdania Markets.

Dickens and the Capital Economics team noted earlier this week that prices of hotel accommodation and airfares fell much more steeply in the U.S. and Japan than they did in Europe last year, for various reasons, and warned that statistical ‘base effects’ would mean that inflation rises sharper in those countries this year than in others.

Inflation fearing investors sold U.S. government bonds while currency traders rushed to buy Dollars following Wednesday’s data although it just so happens that price changes announced this week actually occurred last month and on what was the first anniversary of 2020’s steepest declines for all U.S. inflation metrics.

This means that the figures in question had been predisposed to steep increases from the get-go, increases that could quickly be reversed over the coming months and which would in any case be unlikely to draw a response from the Federal Reserve.

{wbamp-hide start}

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

“The FOMC made it crystal clear they will look through temporary inflation overshoots. In fact, the FOMC seeks to achieve inflation (as measured by the PCE deflator) that averages 2% over time. The PCE deflator has averaged less than 2% for over a quarter of a century,” says Elias Haddad, a senior FX strategist at Commonwealth Bank of Australia (CBA).

“We recommend investors use USD relief rallies to initiate or add to short USD positions.”

Haddad and the CBA team have told clients they should sell into the nascent Dollar rally and use proceeds to buy Canadian, New Zealand and Australian Dollars that offer exposure to rising.

Above: U.S. Dollar index shown at weekly intervals alongside AUD/USD.

Commodities including oil, iron ore and copper have continued to build on already-substantial earlier gains thus far in the year, which has had an uplifting impact on measures of perceived ‘fair value’ and could help to underwrite further increases in connected currencies over the coming months.

The underlying idea is that Fed monetary policy means the Dollar will struggle to sustain its gains irrespective of whether inflation rises further in the months ahead or if it instead begins to recede.

The Fed has said it won’t even countenance changes to its exceptionally accomodative monetary policy unless and until inflation has held above its target long enough for inflation to average the 2% target over an unspecified period of time.

Above: Partial screen grab of Capital Economics’ inflation dashboard.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

“The disinflationary effects of the pandemic were particularly pronounced in the US and inflation in some components will rise mechanically and temporarily as those effects unwind. Inflation in other components may ease, but not by enough to offset those increases. Higher commodity prices will boost inflation temporarily in all advanced economies,” says Capital Economics’ Dickens.

While it may surprise some readers or the world’s more casual economy-watchers, inflation has actually been too low in the U.S. and many other parts of the developed world for at least the last decade, which is why the Fed announced changes to its inflation targeting strategy in June 2020 and now says that it’ll much slower to raise interest rates than in the past.

With official interest rates set to remain near zero for what could be years yet, any periodic increases in price pressures are a potent recipe for imposing deeply negative inflation-adjusted returns on most of the investors who hold U.S. government bonds.

These price increases could also have the effect of indirectly reducing the returns earned by investors in many other U.S. Dollar denominated assets including stocks and so is far from an obvious argument for outperformance by the greenback.

“The extent to which this near-term rise in inflation is sustained will depend strongly on fundamental economic developments. So far, there is most evidence of a rise in underlying price pressures in the US, which is consistent with our forecast of a prolonged upward shift in core inflation there,” Dickens says.