GBP/EUR Week Ahead Forecast: Another Flirt With 1.15 If Big Data Week Goes Awry

- Written by: Gary Howes

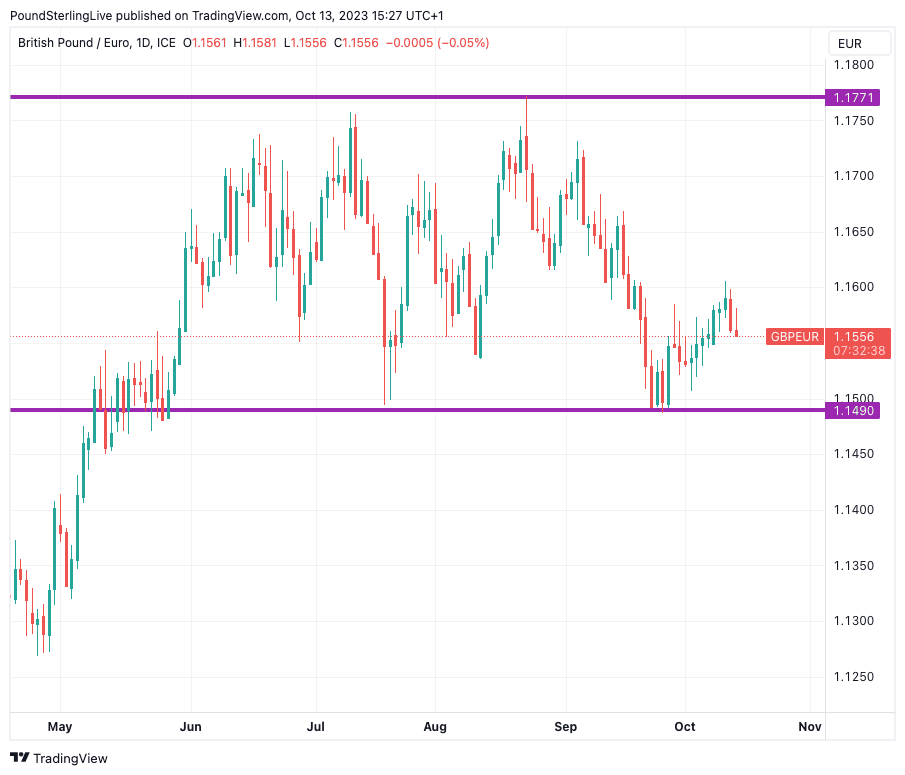

- GBPEUR chart reveals pressures building

- Retest of 1.15 now back on cards

- But, major UK data releases await

- UK wages and employment due Tuesday

- Inflation data out Wednesday

Image © Adobe Images

Pound Sterling looks to be back under pressure against the Euro after a gentle recovery that spanned seven consecutive days was reversed towards the end of last week, interest over the coming days is supplied by UK wage and inflation numbers.

To be sure, the recent recovery seen in the Pound to Euro exchange rate was tepid (it took 13 days to reverse a 3-day fall) and lacked any major impetus and the recent decline puts the pair on course for a retest of the May-October range's lower boundary, which resides in the 1.15 area.

For now, we would not expect this solid source of support to break and see weakness as limited in scope, particularly as the Eurozone economy is no shining beacon of outperformance when contrasted to the UK.

Above: GBPEUR at daily intervals with the confines of a broad range sketched. Set up a daily rate alert email to track your exchange rate OR set an alert for when your ideal exchange rate is triggered ➡ find out more.

Last week's string of daily advances nevertheless offered fledgling evidence that GBPEUR was rebuilding near-term strength and charting a course back to the top of the range towards 1.1650-1.17.

But the late-week turn lower confirms this exchange rate is intent on a random walk within the comfort of its ageing range.

The good news for those looking for some decisive action in this pair is that there are some market-moving events on the UK calendar to look forward to. The coming week is busy for UK data releases and idiosyncratic volatility for Pound exchange rates can therefore be expected.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

"The release of UK labour market, inflation and retail sales data could attract considerable attention. Given the reassessment of the BoE policy outlook by the markets in recent weeks and the aggressive unwinding of GBP-longs, the GBP could benefit from any positive data surprises," says a weekly FX analysis note from Crédit Agricole.

Tuesday sees the release of UK labour market statistics and the market will react to earnings and changes in employment levels as these offer a signpost as to where UK inflation trends could be headed over the coming months.

Average Weekly Earnings - excluding bonuses - are expected to have risen 7.8% annualised, unchanged on a month prior.

But economists at Pantheon Macroeconomics look for a fall to 5.0% annualised, representing a sizeable undershoot that would lower the odds of the Bank of England raising interest rates again, weighing on UK bond yields and the Pound.

Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics, says the labour market report will likely show that the unemployment rate has continued to exceed the Bank of England's expectations and wage growth has started to lose some pace.

Above: UK wage dynamics, courtesy of Pantheon Macroeconomics.

The market expects a 4.3% headline unemployment rate in August, unchanged from July, but above May's 4.0% and the Bank of England's Q3 forecast for 4.1%.

The Bank of England, therefore, shouldn’t hesitate to keep Bank Rate at 5.25% next month, according to Tombs.

Wednesday brings with it the all-important inflation numbers for September and the market looks for headline inflation to fall to 6.5% year-on-year from 6.7% previously, but the month-on-month reading is anticipated to have risen from 0.3% to 0.4%, primarily as a result of rising fuel prices.

September's release proved a decisive moment for the Pound as the unexpectedly soft reading prompted a selloff that endured through the month. Another undershoot could trigger similar price action in October, putting the bottom of the already-mentioned range at 1.15 under notable pressure.

Friday will see the release of GsK consumer confidence figures and retail sales, while offering some interest these releases are unlikely to have a material impact on the market, particularly given the sizeable signals that will have been provided by the wage and inflation numbers just days earlier.

In the Eurozone, German sentiment will be on tap Tuesday at 10:00 BST and markets will be keen to see how Germany's prospects are rated, particularly given the recent deterioration in activity that leads economists at Deutsche Bank to predict a double-dip recession is shaping up.

Wednesday sees final confirmation of the Eurozone's inflation figures and because this is an update to the preliminary release we would not anticipate markets to be too flustered.

All signs point to the European Central Bank (ECB) being ready to pause its interest rate hiking cycle with Governing Council members last week pointing to the importance of Q1 2024 wage data for informing future moves.

The pause on rates does, on balance, deny the Euro support from the interest rate channel, particularly against the likes of the Dollar and Pound whose central banks could yet hike interest rates again in 2023.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes