Pound-Euro Exchange Rate Sheds four Months of Gains in the Space of Five Days

- Global investor sentiment counts for GBP

- Investors are running scared, hammering GBP

- Expectations for Bank of England rate cut rise

Above: File image of the doors to the Bank of England © IRStone, Adobe Stock

- GBP/EUR spot at time of writing: 1.1467, +0.10%

- Bank transfer rates (indicative): 1.1166-1.1246

- FX specialist transfer rates (indicative): 1.1300-1.1364 >> More information

The sell-off in Pound Sterling has been spectacular: the UK currency has shed four months of hard-fought gains - gains that encompassed the signing of a Brexit deal and a landslide election victory - in the space of a mere five days.

And the driver behind the precipitous decline is now clear: the market's coronavirus fears.

The Pound-to-Euro exchange rate had been as high as 1.20 in February, but at the start of January the exchange rate is languishing below 1.15, and the decline appears to coincide with the sizeable sell-off in global stock markets.

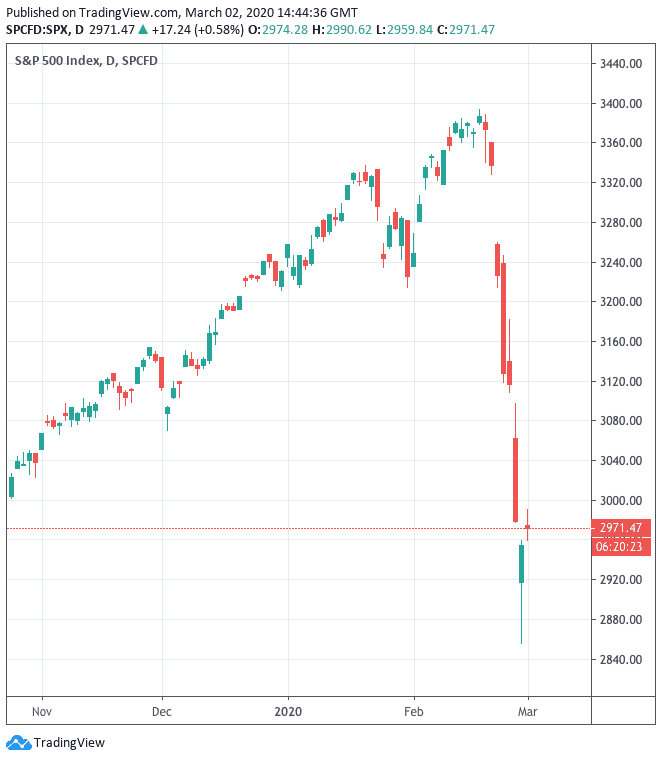

If we look at the price action in the S&P 500 since last week we see the following:

A look at the GBP/EUR exchange rate meanwhile shows the following:

What is the common theme that binds the decline in stocks and the decline in the Pound against the Euro? A fear amongst investors that the coronavirus will deliver a notable blow to global growth.

It is important to note that the UK economy itself might be relatively immune to the economic contagion of the virus, but Sterling is not so immune. This is largely because the Pound is propped up by substantial inflows of global investor capital.

When these inflows dry up - as is the case when investors are running scared of a virus outbreak - the Pound proves to be one of the most vulnerable global currencies.

"Sterling relies on a steady stream of external finance to maintain its value; rising risk aversion will hurt it. Stronger demand for gilts didn't shore up sterling in 2008; outflows from other asset classes will dominate," says Samuel Tombs, UK Economist at Pantheon Macroeconomics.

"The Pound is a structurally weak currency and it remains sensitive to global investors' appetite for risk," adds Tombs.

Markets are currently reflecting a fear that the coronavirus outbreak has further to play out and the economic effects are therefore ultimately not fully known. This kind of uncertainty provides fertile ground for the selling of stocks.

"Although cases have now likely peaked in China, we expect news flow from the rest of the world to get worse before it gets better. We estimate the work resumption rate in China’s industrial sector will accelerate to 73% by the beginning of March from around 35% as of 17 February. (Work is resuming more slowly than we had pencilled in a few weeks ago.) The spread of the virus across Asia, Europe and potentially the US poses further new risks to our forecasts. The huge uncertainties mean this note is about the chances of variance from our current outlook," says Shweta Singh, Managing Director, Global Macro and Europe Economics at TS Lombard.

The Pound is also apparently being weighed down by a spike in expectations for an interest rate cut at the Bank of England this March in response to the prospect of a global economic slowdown.

Bank of England Governor Mark Carney has told Parliament's Treasury Select Committee on Tuesday that the Bank stands ready to provide assistance to the economy in the face of any potential negative impacts of the coronavirus outbreak.

Carney says the Bank of England is, "assessing the economic impacts and considering the policy implications of various possible scenarios... we will come to quick conclusions about the appropriate stance of policy."

We would imagine that any domestic economic impact will be difficult to fathom by the time the Bank's meeting comes about on March 26. Instead, any interest rate cut at the Bank would more than likely be in sympathy with actions at other central banks, as part of a coordinated global response.

Carney told the Treasury Select Committee he is in contact with counterparts in the world’s biggest economies and the International Monetary Fund.

G7 finance ministers are due to hold a conference call on the virus later on Tuesday, detailing any potential coordinated increase in government spending that could help shore up the global economy.

#BoE Gov Carney:

— Michael Brown (@MrMBrown) March 3, 2020

- Will ensure all necessary contingency plans are in effect

- BoE to help economy thru coronavirus shock which will be large but temporary

- BoE will take all necessary steps to help economy

- BoE monitoring situation closely, in frequent contact with intl peers

When expectations for a central bank interest rate cut rise, as is the case with expectations for a rate cut at the Bank of England, the currency that central bank issues tends to fall as ultimately lower interest rates mean an increase in the supply of that currency.

Expectations for a rate cut rose on Monday when a Bank of England spokesperson told Bloomberg that the Bank will take "all necessary steps ... to protect financial and monetary stability. The bank continues to monitor developments and is assessing the potential impacts".

"In the wake of recent rumours regarding global interest rate cuts, the Bank of England may be forced to envisage an easing of monetary policy earlier than previously expected," says Marc-André Fonger, Head of Research at Fongern FX.

However a rate cut is not a done deal, considering the relative resilience of the UK economy. According to the IHS Markit Manufacturing PMI which was released on Monday and shines a light on how the UK's manufacturing sector performed in February, new orders grew at the fastest pace in 11 months and business optimism hit a nine-month high.

However, Rob Dobson, a director at IHS Markit, said the effect of the coronavirus outbreak was starting to make itself felt.

“Supply-chain disruptions were emerging rapidly ... as the COVID-19 outbreak led to a substantial lengthening of supplier lead times, raw material shortages, reduced inventories of inputs, rising input costs and reduced export orders from Asia and China in particular,” said Dobson.

The Bank of England could well lean on such evidence when formulating their policy response on March 26.

We note that the rise in expectations for a Bank of England interest rate cut merely mirror the rise in expectations at other global investment banks: for instance the U.S. Federal Reserve is expected to deliver a whopping 100 basis points of cuts. Therefore, on a relative basis we fail to see why the Pound should be especially hurt by the Bank's developments.

When looking at the Euro, the European Central Bank (ECB) has far less scope than the Bank of England and Federal Reserve to cut interest rates, considering the deposit facility rate is already at -0.50%. When a central bank has interest rates at record lows at the start of an economic downturn it finds that the tools at its disposal to fight that downturn are severely limited.

Hence, the Euro does not face the prospect of deep interest rate cuts as does the Pound and Dollar which is a key factor behind the GBP/EUR fall of late.