GBP/NZD Week Ahead Forecast: GBPNZD Staying Bullish, Eyes on Key UK Risk Events

- Written by: Gary Howes

- GBPNZD sees 2023 high close by

- Technical studies remain bullish

- UK inflation and Bank of England pose two-way risk

- Westpac says peak in GBPNZD is at hand

Image © Adobe Stock

The uptrend in the Pound to New Zealand Dollar (GBPNZD) remains valid according to most technical studies, however, a break of 2023's highs could yet prove elusive if this week's event risks go against Sterling.

Risks to the rally come in the form of Wednesday's UK inflation data release and Thursday's Bank of England decision, confirming the focus for the pair lies on the GBP side of the equation over the coming days.

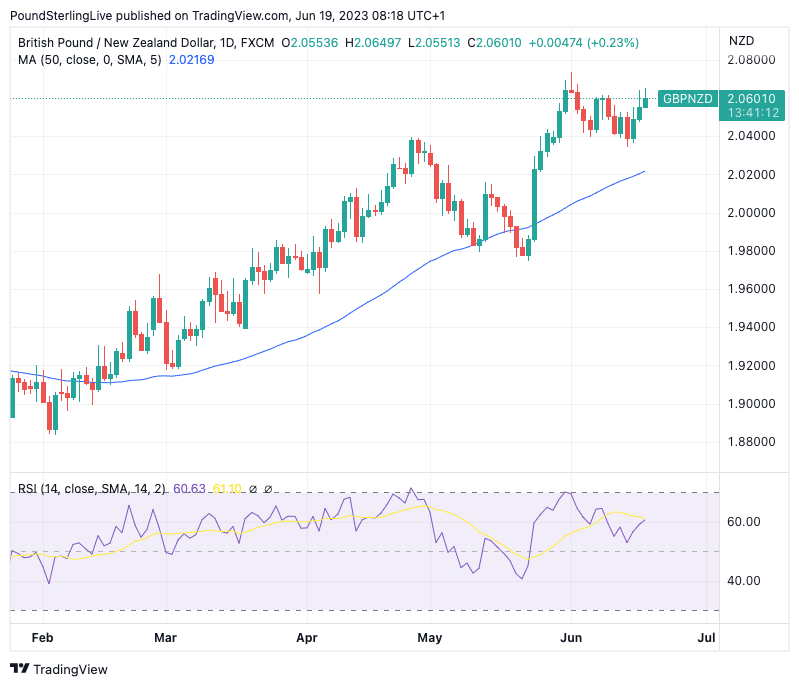

The two calendar risks come amidst an intact uptrend in GBPNZD that took it back to 2.0648 on Monday, less than 100 pips shy of 2023's high at 2.0738.

To be sure, the broader 2023 rally stalled in June but has since picked up again over the course of the past week.

The run-up into 2023's high, which was reached back on June 01, could yet be met with selling interest as such multi-year peaks can become psychologically significant technical levels.

A retest of 2.0738 is an achievable objective for NZD buyers near-term but the market would likely need a fresh upside impulse in buying interest to crack this ceiling.

Despite the likely defences lined up around 2.0738, basic technical studies are still broadly supportive of further GBPNZD upside: momentum remains positive with the Relative Strength Indicator on the daily chart reading at 67, which puts it above neutral but below an overbought reading of +70.

The pair is also above its 50-day moving average which denotes the persistence of upside pressures.

Above: GBPNZD at daily intervals with the 50-day moving average and RSI indicator (lower) panel.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

GBPNZD gains come as the New Zealand Dollar has struggled over recent months amidst signs of an economic slowdown in New Zealand, indeed last week a recession was confirmed thanks in part to elevated central bank interest rates.

The Reserve Bank of New Zealand's (RBNZ) recent guidance that it would likely now pause the hiking cycle has meanwhile left the NZD without support from the interest rates channel as the perceived peak leaves investors free to bet on interest rate cuts further out.

"In New Zealand, GDP growth contracted for two consecutive quarters. The fall in output is earlier than RBNZ’s forecast of a technical recession by Q3’23. However, wages and food inflation continue to remain high. On balance, the fall in output gives the central bank reasonable confidence to maintain its OCR forecasts, since the policy rate is now highly restrictive and output growth is negative. Currently, we stay neutral on NZD," says Antony George, G10 FX Strategist at NatWest Markets.

Turning to the UK, Pound Sterling has been boosted of late by rising short-term UK bond yields which in turn reflect expectations for further Bank of England rate hikes, owing to the UK's 'sticky inflation' problem.

Therefore the immediate risk to the Pound Sterling uptrend lies with the CPI inflation report on Wednesday, June 21 where a downside miss could see Bank of England rate hike expectations deflate, which would prompt an unwind in GBP strength.

The Bank of England then delivers its next hike the following day on June 22 and could introduce some 'dovish' guidance on any inflation undershoot; after all the Bank will be eager to bring an end to its hiking cycle to avoid prompting a deep recession.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes

Another downside risk to GBPNZD would involve inflation coming in well above expectations, a counterintuitive position to what has already been written above regarding the impact of below-consensus inflation.

Such an inflation blow-out could prompt a surge in bond yields (which pushes up mortgage rates and the cost of borrowing elsewhere) and raises the prospect of a deep recession forming at some point in the coming months.

Such an outcome could therefore be considered negative for the Pound.

So for the immediate term, an on-target inflation print would likely be required to underpin the Pound's uptrend against the New Zealand Dollar.

Elsewhere, economists at Australia and New Zealand lender Westpac have updated their New Zealand Dollar forecasts to show the peak in GBPNZD has likely been met and a trend of depreciation that will last into 2024 is now at hand.

The bank's New Zealand-Pound forecast profile shows 0.49 for end-September, 0.49 for year-end, 0.49 for end-March 2024 and 0.50 for end-June 2024.

This gives Pound-New Zealand Dollar profile of 2.04, 2.04, 2.04 and 2.0.

Compare GBP to NZD Exchange Rates

Find out how much you could save on your pound to New Zealand dollar transfer

Potential saving vs high street banks:

NZ$5,350

Free • No obligation • Takes 2 minutes