Euro-Dollar Week Ahead Forecast: Retesting 1.19 after Recovery Sprouts, Coronavirus Ebbs

- Written by: James Skinner

- EUR/USD eyeing 1.19 as European horizon brightens

- Perking up after economy exits first gear & virus ebbs

- EZ economy outpaced U.S. in Q2 & could rally further

- But lingering enthusiasm for USD limiting EUR upside

Image © Adobe Images

- EUR/USD reference rates at publication:

- Spot: 1.1885

- Bank transfers (indicative guide): 1.1467-1.1550

- Money transfer specialist rates (indicative): 1.1776-1.1800

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Euro-to-Dollar exchange rate entered the August month close to four-week highs and with scope to retest if-not reclaim the 1.19 handle over the coming days now the Eurozone economy has shifted into second gear and the coronavirus has entered retreat across large parts of the continent.

Europe’s single currency shook hands with 1.19 on Friday before ebbing ahead of the weekend though could recover the level this week if the Dollar remains soft and the market comes to recognise the inflection point upon which the Eurozone economy currently stands.

This is after Eurostat data revealed amid month-end trading on Friday that the Eurozone economy grew faster than even the U.S. economy when exiting recession last quarter, more-than drawing a line under the -0.3% contraction seen in opening months of the year.

“Euro area real GDP increased by +2.0%qoq (non-annualised) in Q2, materially above consensus expectations,” says Nikola Dacik, an economist at Goldman Sachs, writing in a Friday note.

Even after subtracting that earlier -0.3% decline, Eurozone GDP growth still roughly matched the pace of expansion seen in the world’s largest economy across the pond and what’s more, some economists suggest that the best is yet to come from the old continent.

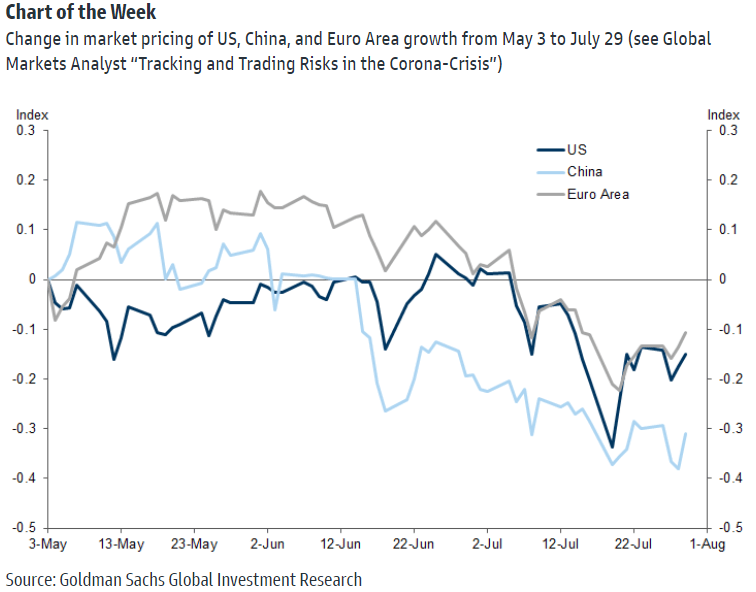

Above: Market expectations for Eurozone, U.S. and Chinese GDP growth trends.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

"We expect an even larger rise (2.8% q/q) in Q3 consistent with real GDP returning to pre-crisis levels by Q4. Inflation also surprised to the upside in July; we see risks to our 3.1% y/y peak forecast for November as skewed to the upside," says Christian Keller, head of economic research at Barclays.

Europe’s GDP growth surprised strongly even with manufacturing sectors in major industrial economies like Germany operating at still-substantially reduced capacity due to supply chain disruptions that have left some firms short of key components and materials.

“We see that order books have never seen as rapid an inflow as in June. The same holds true for export expectations over the months ahead, which have never been improving this quickly. Manufacturers are expecting to profit from the global upturn as Covid-19 retreats. This illustrates that despite all the disruptions for manufacturers, the outlook remains very bright,” say Bert Colijn, a senior economist at ING.

And as these production headwinds fade the bloc’s economy would almost inevitably receive a further tailwind, at a time when many economists also expect the services sector to be going from strength-to-strength as consumer facing businesses recover from earlier closures and restrictions.

“The recovery in the services sector should be sustained in the coming quarters, on the back of rising vaccination rates and the accompanying gradual return to normal (58% of the EU population has had at least one shot and 48% is fully vaccinated). In addition, uninterrupted strong order books in the manufacturing sector, improving global trade and the Next Generation EU support the outlook,” says Maartje Wijffelaars, an economist at Rabobank.

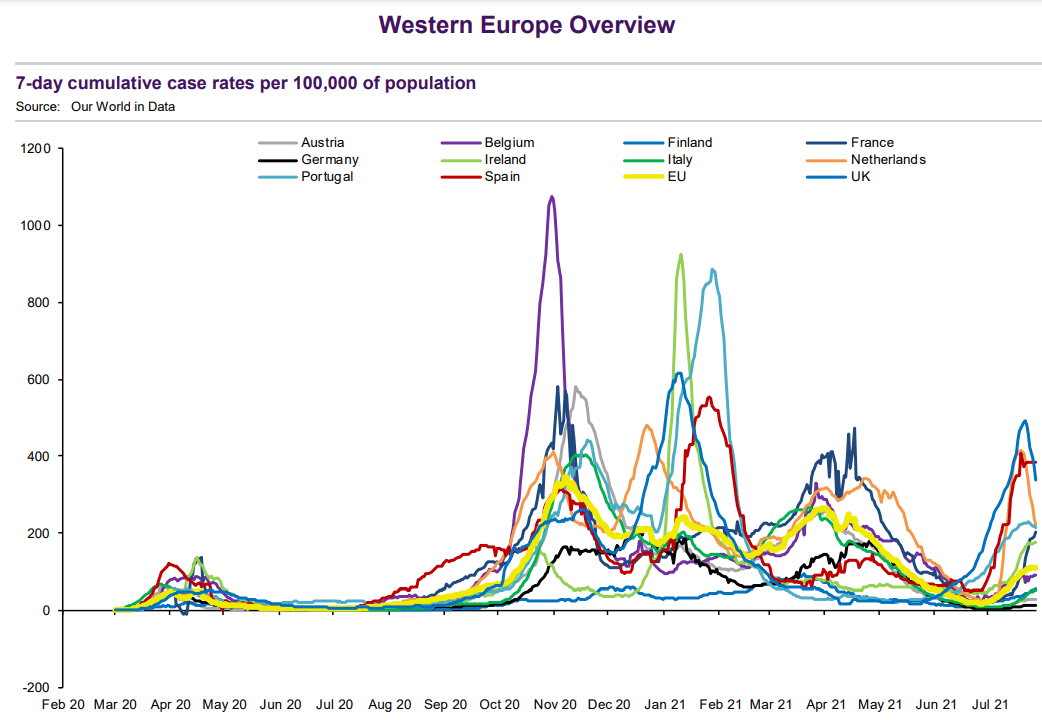

Europe’s economic performance has improved and the outlook for it is brightening amid increasing coronavirus vaccine availability, rising uptake and what are for many major economies on the continent, falling numbers of coronavirus infections.

Above: Coronavirus trends in Western European economies. Source: Natwest Markets.

“The peak may be behind us in the worst affected countries. Early data suggests case rates in some countries that have had worryingly high instances of the Delta variant (UK, Spain, the Netherlands) have peaked,” says Imogen Bachra, a European rates strategist at Natwest Markets.

“Markets are cautious, but we think this scare should be temporary. We are optimistic that the turn in case rates, as well as the weakened link between case rates and hospitalisations and mortality rates thanks to the vaccine should feed through to a shift in market narrative. But, this may not be immediate. Ultimately, we still see higher yields, but it may take a few weeks and more evidence of positive covid news,” Bachra says.

Europe’s unified unit tested 1.19 in the final session of last week even as the Dollar pared earlier losses against other currencies, indicating increased interest from the market, which could grow further if the Dollar remains reluctant to appreciate and the economic outlook continues to brighten.

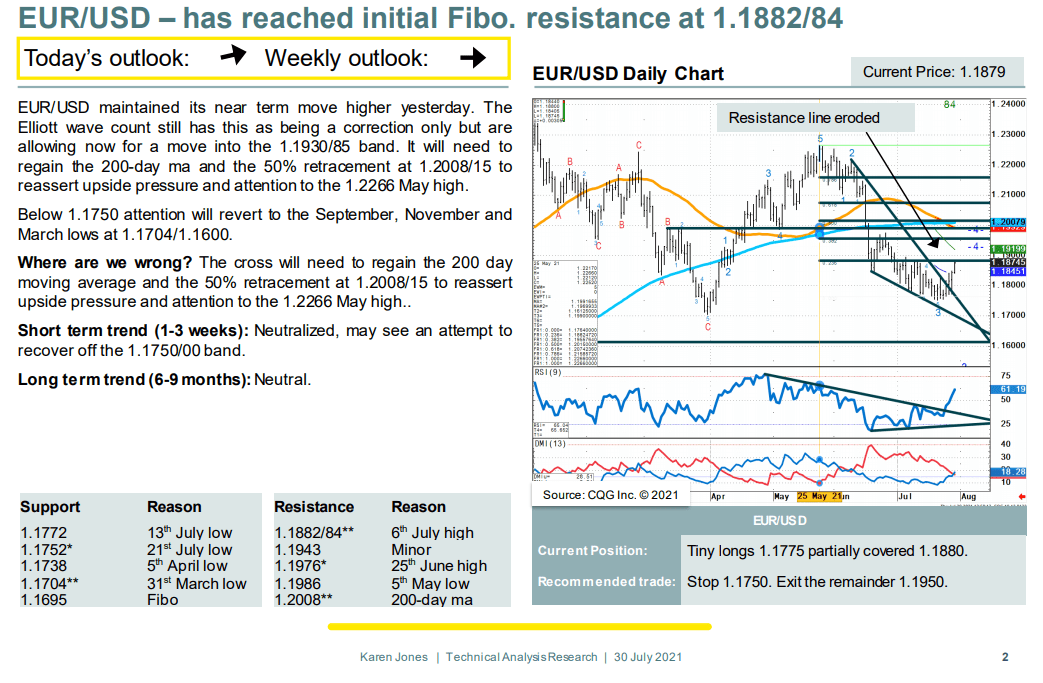

Meanwhile, the charts continue to suggest there’s a thicket of support levels to underpin the Euro 1.1700 and and 1.1772 while some technical analysts see it having scope to rise as far as 1.1950 over the coming days.

Above: Commerzbank technical slide from Friday, 30 July.

{wbamp-hide start}

{wbamp-hide end}{wbamp-show start}{wbamp-show end}

“The Elliott wave count still has this as being a correction only but we are allowing now for a move into the 1.1930/85 band. It will need to regain the 200-day ma and the 50% retracement at 1.2008/15 to reassert upside pressure and attention to the 1.2266 May high,” says Karen Jones, head of technical analysis for currencies, commodities and bonds at Commerzbank, referring to EUR/USD.

Much depends on the trajectory of the Dollar however, although this has generally weakened since last Wednesday’s Federal Reserve (Fed) monetary policy decision that saw the bank indicate that it’s only plodding toward a tapering of its $120BN per month quantitative easing (QE) programme, at a slower place than the market had anticipated and in what is potentially an ongoing headwind for the greenback.

Nonetheless, July’s non-farm payrolls report is due at 13:30 onFriday and it’s possible the prospect of a strong number in line with or better than the 895k consensus could limit enthusiasm for the Euro over the coming days, though analysts at MUFG have noted a burgeoning trend that has seen economists overestimating the likely pace of job growth and in the process leaving the Dollar vulnerable to declines following the announcement.

“The [Dollar Index] reaction to previous nonfarm payroll reports is clear – the tendency for the dollar to weaken is quite strong. In the last eight NFP releases, the dollar has weakened one hour later on seven of those times – an implied 88% probability. This reflects the fact that markets position for very strong job growth which fails to meet expectations,” says Lee Hardman, a currency analyst at MUFG.

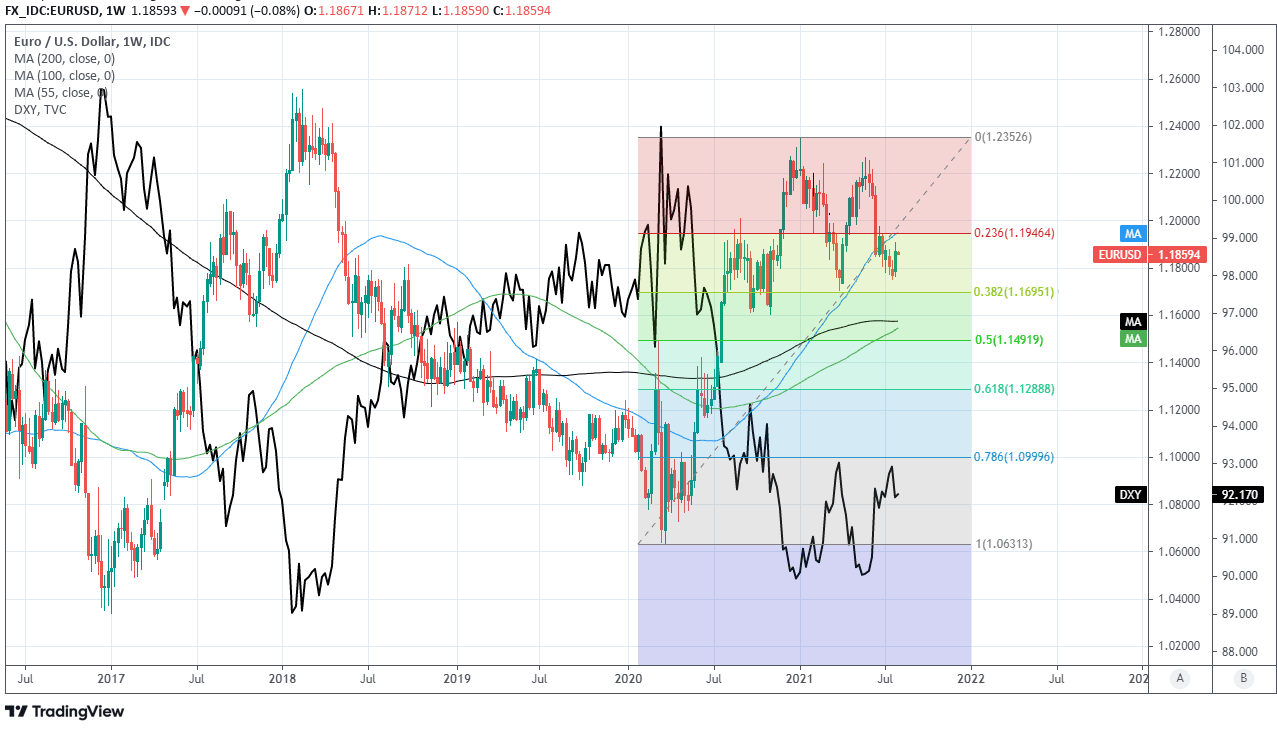

Above: Euro-to-Dollar rate shown at weekly intervals alongside U.S. Dollar Index. Includes Fibonacci retracements of 2020 recovery trend and key moving-averages.