Euro-Dollar Week Ahead Forecast: Eyeing 1.22 as USD Blinks in Fed Stare Down

- Written by: James Skinner

- EUR/USD has 1.22 in the crosshairs this week

- USD fall sparks global rally, raising EUR

- Global economy shows signs of improvement

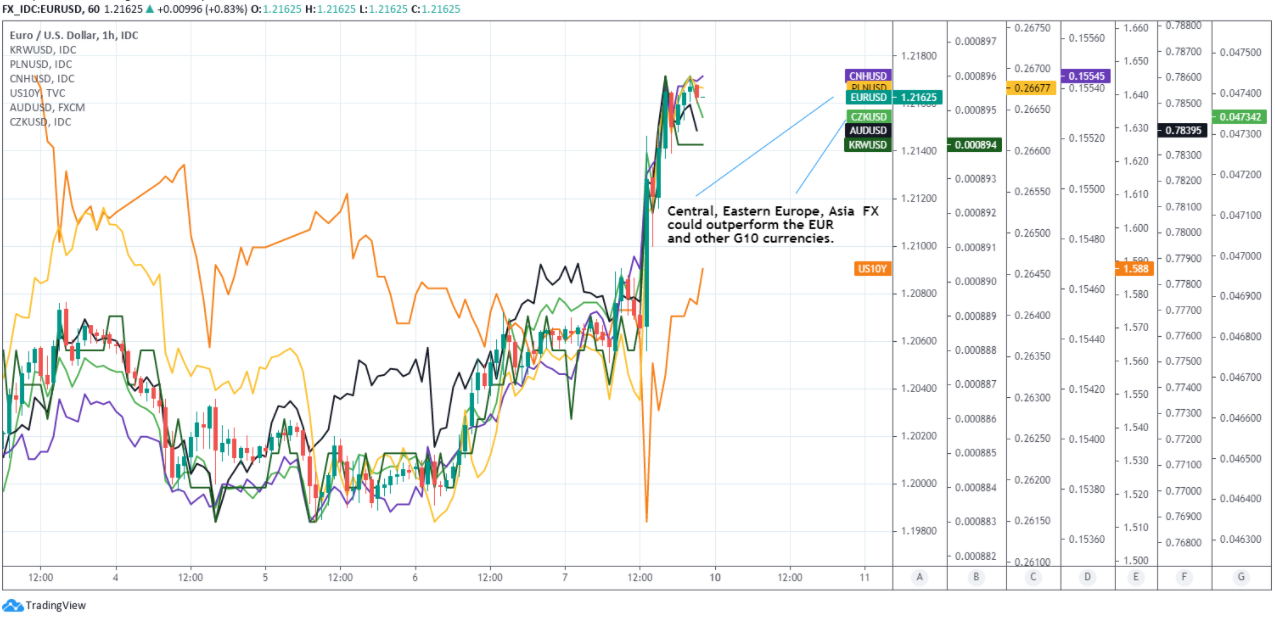

- CEE, Asia may outperform EUR, other majors

- Opportunity in PLN, CZK, RUB, KRW, MYR et al

Image © Adobe Images

- EUR/USD spot at publication: 1.2157

- Bank transfer rates (indicative guide): 1.1730-1.1817

- Money transfer specialist rates (indicative): 1.2071

- More information on bank-beating rates, here

- Set a rate alert, here

The Euro-to-Dollar exchange rate entered the new week near its late February highs but could reclaim further lost ground over the coming days now that the global economy is showing signs of shifting into a higher gear and the market has blinked in an attempted stare down of the Federal Reserve.

Dollars have been sold and Euros bought heavily since April’s non-farm payrolls data vindicated the Federal Reserve (Fed) for its insistence that the U.S. economy remains a long way off from the job and inflation targets the bank wants to achieve before it entertains changes to its globally supportive monetary policy.

U.S. job growth was nothing to be sniffed at however, given that before pandemic times a 266k payrolls increase would have been celebrated as a blockbuster in some parts of the market even if it was not enough on Friday to satisfy lofty expectations of both the market and the Fed.

“It likely relieved some pressure from the Fed to shift to a less dovish rhetoric. At the same time, the data-miss was not enough to severely dent the underlying recovery story, leaving the global risk sentiment broadly supported,” says Chris Turner, global head of markets and regional head of research at ING.

Gains fell well short of the nearly 1 million new jobs anticipated by consensus but still sent a clear signal that U.S. growth is recovering strongly enough to provide a shot in the arm to other economies elsewhere in the world.

This is a boon for currencies like the Euro.

Above: EUR/USD at daily intervals with Fibonacci retracements of January decline and U.S. Dollar Index (Green).

This week is a quiet one for major European economic data but will see April’s inflation and retail sales numbers released in the U.S., although neither could dislodge the Fed from its lower-for-even-longer-than-ever-before interest rate stance, nor do many see them pulling the Dollar from its renewed downward trajectory.

Fed policymakers have set a high bar including "substantial further progress" toward pre-pandemic levels of employment and a stronger as well as more sustained rate of inflation than they’ve ever sought to generate with monetary policies before as prerequisites for changes to quantitative easing and interest rate policies.

Many analysts say this is an argument against holding the Dollar in any event and more so now given the Eurozone and rest of the global economy are tentatively showing signs of shifting into a higher gear, which is doubly supportive of the Euro-Dollar outlook.

“We continue to favour EUR/USD longs as an expression of broad Dollar depreciation, due to improving domestic fundamentals for the Euro Area. After a slow start, the EU vaccination program is now going even faster than we’d expected, and our Global Economics team now estimates that the EU will match the US by vaccinating 50% of the population around mid-June,” says Zach Pandl, co-head of global foreign exchange strategy at Goldman Sachs.

The Eurozone economy contracted less than was expected in the first-quarter while surveys of conditions in key industries have pointed toward a rebound from April.

However, it’s Dollar downturn and impact it had on other currencies that was in the driving seat of the Euro-Dollar rate last week and which could remain so for the time being.

Above: Euro-Dollar rate shown at weekly intervals with Renminbi-USD exchange rate.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

“China's goods trade surplus with the US has nearly doubled from $15bn in the space of just two months (according to China Customs data), since the end of February,” says Stephen Gallo, European head of FX strategy at BMO Capital Markets, referring to Chinese trade balance data released in the early hours of Friday.

“While we're conscious of the fact that RMB rates and Chinese A-shares are trading in a subdued manner, the path towards levels just below 6.40 in USDCNH is clearer,” Gallo adds.

China’s surging goods trade surplus with the U.S. reflects a profitable export business that will have knock-on effects for other economies in Asia, Europe and elsewhere in the world.

This is a part of why the Renminbi is strengthening against the Dollar, which is often a supportive influence on EUR/USD while both of these often tend to have uplifting impacts on other currencies within their respective regions though notably South East Asia as well as Central and Eastern Europe.

Many currencies in those regions have underperformed over the last year and their economies are showing signs of recovery; making them natural candidates for outperformance in the short-term including against the Euro.

Included among those are the Korean Won, Malaysian Ringgit, Singapore Dollar, Russian Rouble, Polish Zloty, Romanian Liev and Czech Koruna, many of which saw had economies that saw renewed outbreaks of coronavirus in the opening quarter or were seen as adversely impacted by vaccine procurement troubles.

Above: EUR/USD at hourly intervals with various Asia Pacific, CEE exchange rates & 10-year U.S. bond yield (orange).

“We expect EUR/PLN to trend lower and outperform HUF & CZK, with Poland’s cum. growth over 2020-2022 to outpace that of EZ/HU/CZ and the market’s still short PLN positioning posing an upside risk to PLN,” says Daria Parkhomenko, a strategist at RBC Capital Markets.

In Central and Eastern Europe Poland’ has proved more resilient to the latest coronavirus containment measures, inflation has surged above the Bank of Poland target and policymakers have indicated they may be willing to consider lifting interest rates next year; much sooner than the Fed, European Central Bank (ECB) and others.

Poland’s Zloty was an underperformer throughout the early stages of this year but outpaced the Euro and others by a country mile on Friday, and likewise with, which also has a brightening economic backstory.

Similar is true of the Russian economy, which also benefits from an elevated oil price, and Czechoslovakia with its Koruna while over in Asia it emerged in late April that South Korea returned to pre-coronavirus levels of GDP last quarter and Singapore surprised on the upside of expectations.

“The Korean won’s performance has been disappointing. Mounting US yields and equity outflows weighed heavily on the won last quarter, though South Korea’s AA-rated bonds continued to entice foreign investors. The won’s rally since mid-March has been tepid however even as the equity outflow ended,” says Alvin Tan, an RBC colleague of Parkhomenko.

“Given the robust fundamentals, KRW could bounce back quickly if and when the US bond market settles down further. There will likely be good opportunities to go long the currency in the current quarter,” Tan adds.