U.S. Job Losses Near 30mn as Coronavirus Threatens a 13% Unemployment Rate for April

- Written by: James Skinner

Image © Adobe Stock

- GBP/USD spot at time of writing: 1.2342

- Bank transfer rates (indicative): 1.2012-1.2098

- FX specialist rates (indicative): 1.2159-1.2233 >> More information

U.S. job losses slowed again last week, Department of Labor data revealed Thursday, but nearly 30 million Americans have made welfare claims since the coronavirus gained a foothold in the world's largest economy.

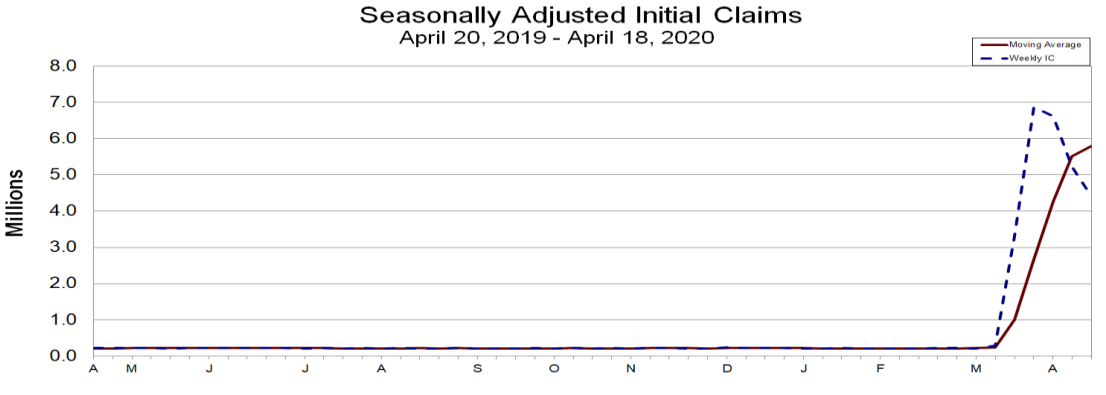

New unemployment insurance claims were 4.42 million last week, down from a downwardly-revised 5.23mn in the prior week but higher than the 4.35mn anticipated by the market consensus. However, and in total the initial claims number has risen by around 27mn since the week ending March 21 and more than 20mn in the April month alone, amid a collapse of the labour market that's threatening to lift the unemployment rate to Great Depression era highs.

"The Department of Labor is continuing to provide guidance and support to the States as they implement the enhanced unemployment benefits under the CARES Act, with 44 States now paying the $600 additional weekly benefit provided by the Act," says Eugene Scalia, secretary of labour.

Continuing insured unemployment claims were 15,97mn, up from 11.9 million the prior week and lifting the insured unemployment rate to a new all-time high of 11%. That's almost double the 7% peak set back in May 1975 although the increase could potentially be understating the spike in the official unemployment rate, which is published by the Bureau of Labor Statistics alongside the non-farm payrolls report on the first Friday of each month.

Above: Department of Labour graph showing initial claims at weekly intervals and moving-average of weekly numbers.

"With these data covering the payroll survey week, we now know that there has been a cumulative 26mn initial jobless claims made since March's survey period, accounting for 17% of the previously employed population," says Andrew Grantham, an economist at CIBC Capital Markets. "With continuing claims once again not rising quite as much as expected and as such suggesting some of the claims have been short-term in nature, we've clearly still seen a dramatic and historic weakening of the economy."

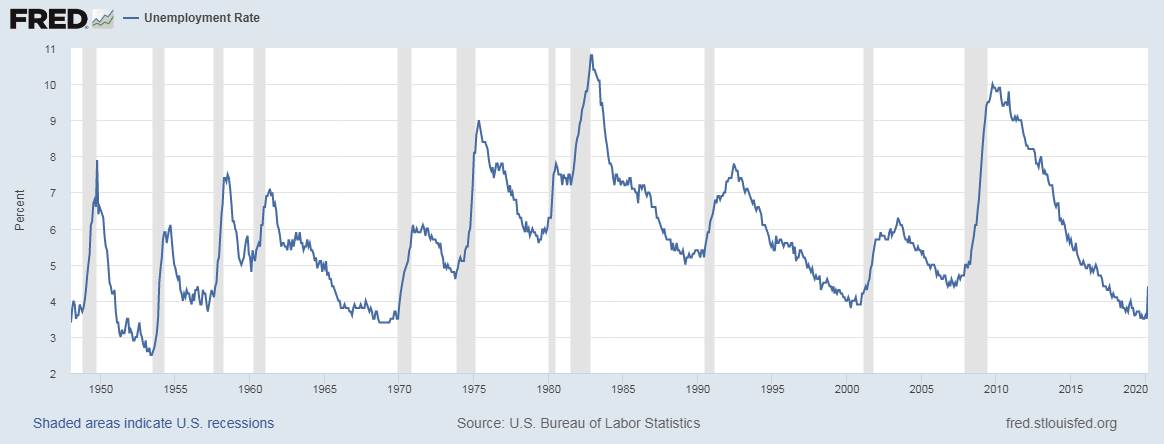

The U.S. had an official unemployment rate of 4.4% as of the end of March when the Bureau of Labor Statistics said there were 7.1mn people classed as unemployed, which would imply an April unemployment rate of more than 20% if all of the new initial claims reported by the Department of Labor were to be converted into continuing claims and subsequently baked into the official rate of unemployment alongside last month's 7.1mn unemployed. But not all initial claims do find their way into the unemployment data.

There have been nearly 27 million initial claims since late March but the continuing claims number has risen from 1.8mn to only 15.9mn in that time, suggesting that at least some newly redundant workers have since found new employment, or given up on their claims. CIBC's Grantham tips an April unemployment rate of 12%-to-13% as a result of this, while Thursday's continuing claims imply a jobless rate of around 13.8% if March unemployment levels and labour force 'participation' levels remain constant this month.

"Another horrendous number, but at least the trajectory is clearly downwards," says Ian Shepherdson, chief economist at Pantheon Macroeconomics. "Our tentative forecasts now are that April payrolls will be reported down about 21M, with May down about 9M. June will depend on how far states are able to re-open their economies, especially in the discretionary consumer services sector, where most of the first wave of jobs disappeared after the lockdowns."

Above: U.S. unemployment rate January 1948 to March 2020. Recessions shaded in grey. Federal Reserve Bank of St Louis.

The White House has set out guidelines for states reopening local economies from various degrees of shutdown but the uneven spread of the virus across the country and its concentration in major urban areas with high population density means there's uncertainty about the pace at which life can return to normal, which is what matters most for the labour market. Although some of the repair may also depend in part on other countries also returning to normal.

Daily increases in U.S. coronavirus infections appeared to reach their peak in early April while officials in New York, the epicentre of the U.S. outbreak, have also acknowledged that the hub of global finance is also over the peak of its own epidemic. Meanwhile, Johns Hopkins University data suggested on Thursday that the number of new infections declared globally each day has also continued a staggered decline since April 12.

Now the focus among analysts, economists and markets is on which economies can reopen and how soon, if at all, they can return to normal. Economists will be watching closely for clues on the likely length of time required for a labour market recovery while epidemiologists will be on the lookout for signs of a second wave or resurgence of infections that would risk augering a fresh shutdown and more pain for economies and labour markets ahead.

"It will be interesting to see what happens in the states that are re-opening parts of their economy from this weekend – Georgia, Tennessee, South Carolina and Florida. We would assume jobless claims will fall back sharply here, but if consumers remain reluctant to go shopping or visit a restaurant due to lingering Covid-19 fears, then employment is not going to rebound quickly. As such it would be another signal that a V-shaped recovery for the US economy is highly unlikely," says James Knightley, chief international economist at ING.