Pound-Dollar Rate Sinks on U.S. Inflation Blowout

- Written by: Gary Howes

-

- U.S. inflation grows 5.4%

- USD rallies in wake of release

- Fed rate rise now likely in 2022 says analyst

Image © Adobe Images

- GBP/USD reference rates at publication:

- Spot: 1.3836

- Bank transfers (indicative guide): 1.3452-1.3550

- Money transfer specialist rates (indicative): 1.3711-1.3740

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Dollar was up sharply against major peers following the release of U.S. inflation numbers that were significantly stronger than expected.

U.S. CPI inflation rose 5.4% year-on-year in June, a sizeable beat on the 4.9% that the market had been expecting.

CPI rose 0.9% month-on-month in June which was ahead of the 0.5% expected by markets while Core CPI rose 4.5% year-on-year, higher than the 4.0% expected.

Investors sold U.S. government bonds and stocks and bought dollars in anticipation of a more aggressive Fed response to rising prices.

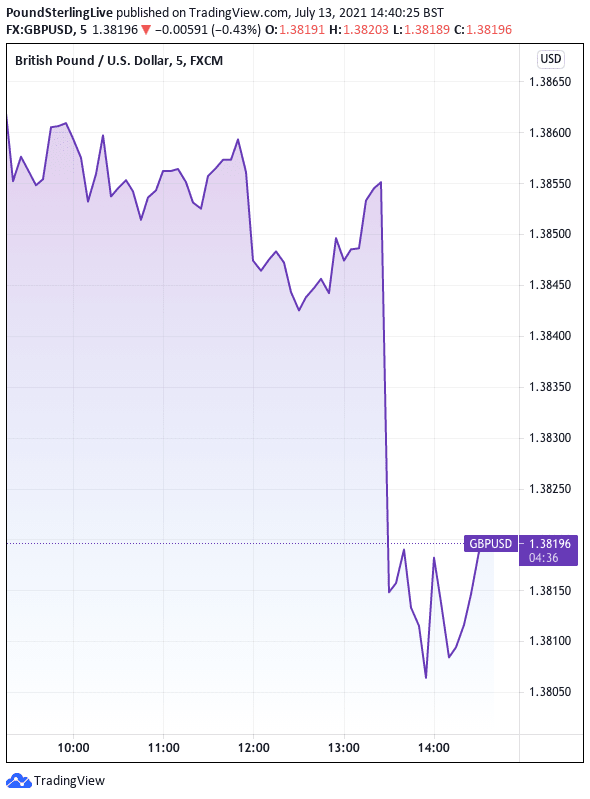

The Pound-to-Dollar exchange rate (GBP/USD) slumped by half a percent in the wake of the release to quote at 1.3817 while the Euro-to-Dollar exchange rate (EUR/USD) fell by a similar amount to quote at 1.1807.

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

"The latest US inflation report came in well above expectations and the markets have reacted by sending the dollar higher and indices lower," says Fawad Razaqzada, Market Analyst at ThinkMarkets.com.

"The jump in CPI was obviously unexpected, given the market’s reaction," he adds.

The data suggests inflation is bound to run ahead of expectations held at the U.S. Federal Reserve and markets are betting the ending of quantitative easing and the first interest rate rise will inevitably be brought forward.

The Fed has a mandate to ensure price stability in the vicinity of 2.0% and raising interest rates would act as a neccessary handbrake to cool inflation.

The prospect of higher interest rates is attractive to international investors seeking higher returns, which in turn bids the value of the Dollar higher.

However higher interest rates act as a handbrake to economic activity and the Fed is loathe to raise rates before U.S. unemployment has fallen to pre-pandemic levels.

"Yet another blowout inflation reading makes it increasingly difficult for the Fed to stick to its position that elevated inflation readings are merely transitory," says James Knightley, Chief International Economist at ING.

Fed Chairman Jerome Powell will be asked to account for his views on inflation and the future of U.S. interest rates when he appears before Congress midweek.

This testimony forms the next significant calendar event for Dollar exchange rates.

"The Chairman of the Federal Reserve, along with his colleagues, has consistently argued that any elevated inflation readings coming out of the COVID recession would be merely 'transitory' as supply chains and shortages worked their way through the system," says Matt Weller, Global Head of Market Research at FOREX.com.

Weller says that while Powell's view could still be right, it doesn’t mean this week’s testimony to an uneasy Congress will be any easier.

"With the cost of transport also rising and oil prices remaining elevated, there is a risk that inflation could remain stubbornly high for a lot longer than the Fed envisages. This is also the fourth consecutive month of above-forecast inflation on both the headline and core fronts," says Razaqzada.

{wbamp-hide start}

{wbamp-hide end}{wbamp-show start}{wbamp-show end}

June inflation was boosted by a big rise in prices of used cars and trucks, which will likely prove transitory.

Ian Shepherdson, Chief Economist at Pantheon Macroeconomics does caution against an overhyped reaction to the data.

He points out that core inflation excluding used cars was in fact 2.7% which looks a great sight less dramatic.

(Core inflation is the component of the CPI reading that excludes global variables such as fuel. In short this is the kind of inflation that matters to the Fed as it is this section of the price basket that would be reactive to rising interest rates).

However Sarah House, Senior Economist at Wells Fargo Securities, says there is increasing evidence that inflation is broadening out beyond categories at the centre of the reopening.

"Food prices rose 0.8% during the month as both restaurant owners and grocers contend with a higher cost environment and are increasingly passing costs onto consumers," says House.

She observes too that agriculture commodity prices remain near a decade high, while average hourly earnings at restaurants have soared recently.

Wells Fargo expects food to remain a major driver of inflation over the next few months and to offset some of the easing in autos and travel services

Shelter inflation is also heating up note Wells Fargo, although the 0.5% increase in overall shelter can be tied to a 7.0% gain in lodging or hotel fares, owners-equivalent rent (OER) has turned higher and rose another 0.3% in June.

"We still expect that inflation will not easily revert to the subdued environment of the mid-to-late-2010s, however. The rapid rise in wages the past few months will likely further encourage businesses to hike prices," says House.

The Fed currently guides that the first interest rate in the upcoming cycle will be required in 2023 but markets simply no longer believe this is sustainable given existing economic dynamics.

"Pipeline cost pressures continue to build and corporates are looking to pass them onto customers in an environment of such robust demand. The case for a 2022 rate hike is strong," says Knightley.

The data and Fed rate hike expectations remain consistent with the current trend of Dollar appreciation and the GBP/USD exchange rate is therefore likely to remain under pressure over coming days.

However, economists at Wells Fargo say despite another surprisingly strong print, the June inflation report still is unlikely to sway Fed officials in their thinking on inflation.

If correct then the market might be guilty of an overreaction, in which case the Dollar might need to readjust to lower levels at some point in the near future.