Eurozone Banks Plummet: "Bloodbath, if you will" says City Index

- Written by: Fawad Razaqzada, Analyst at City Index

-

Image © Adobe Stock

After a day of relative calm, concerns over financial stability intensified at the start of Wednesday’s session.

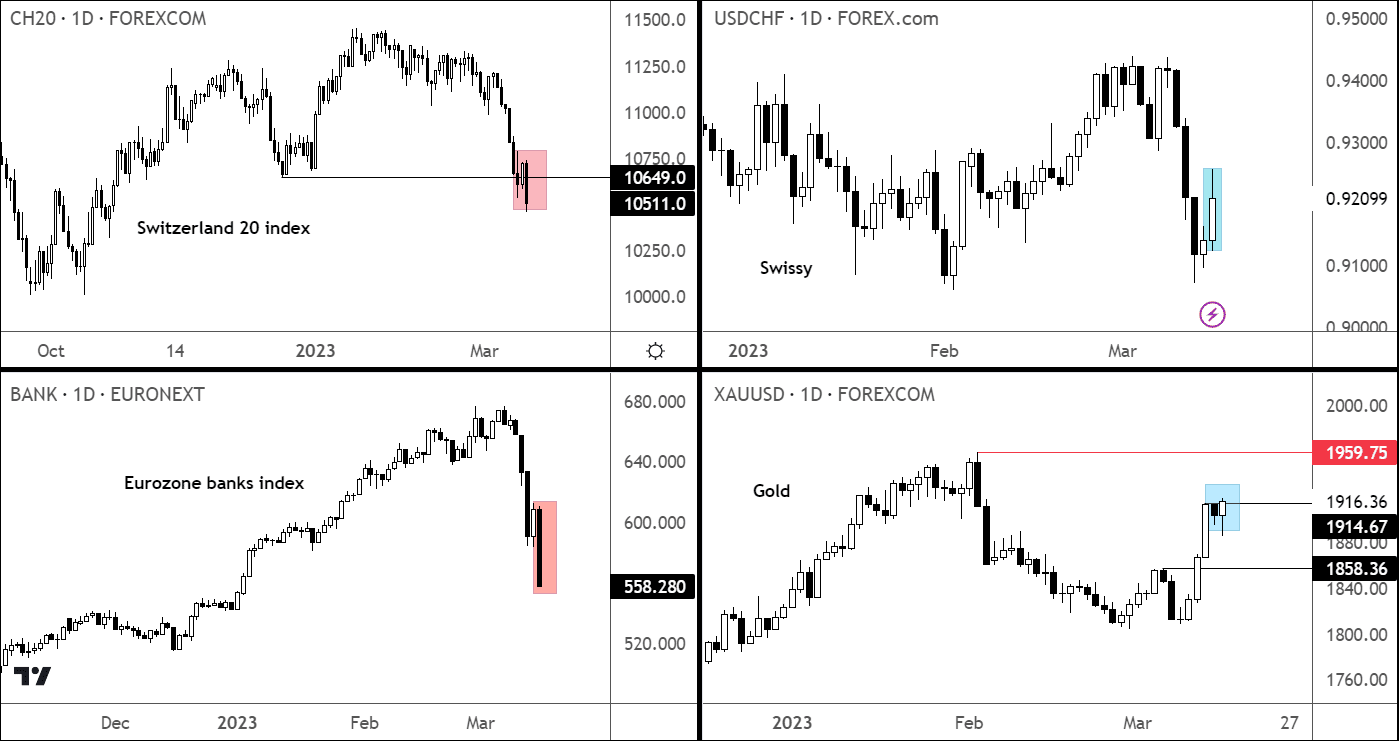

Shares in European banks got an absolute hammering after Credit Suisse plunged more than 20% to a new record low. An index of European bank stocks fell 5%, while the Euro Stoxx 50 volatility hit its highest since October.

You get the picture: investors were panicking. Bloodbath, if you will.

This comes fresh on the heels of a broader industry selloff following the collapse of Silicon Valley Bank. Concerns over another 2008-style financial crises have intensified.

The selling of financial stocks was triggered by Credit Suisse, which has seen its shares hit repeated all-time lows in recent weeks.

The lender's biggest shareholder, Saudi National Bank, announced it could not raise its stake more than 10% in the beleaguered Swiss bank because of regulatory issues.

Concerned by another bank failure, traders sold shares of European banks heavily.

Barclays, Deutsche, BNP, SocGen et. al., were showing losses of around 8-10% each as investors worried about their exposure to the Swiss lender.

Image courtesy of City Index.

In FX, the euro and Swiss franc both dropped sharply.

More loses could be on the way if investor concerns over Credit Suisse is not addressed by authorities quickly. If the bank fails, this could have major implications for other European banks that have exposure to the beleaguered Swiss lender.

The EUR/USD could easily drop back below 1.05 handle, with investors now not too sure whether the ECB will opt for that 50-basis point rate hike that they had built up so much.

Thanks to another sell-off in stock and bond markets, gold shone brightly, again, although there was not much enthusiasm for Bitcoin and cryptos this time.

WTI dropped below $70 to its weakest point since December 2021. Precious metals could expand their gains as investors continue to price in the probability of rate cuts towards the end of the year and reduce expectations of further monetary tightening.