Indian Rupee is Set to Rise after Inflation Stops RBI in Tracks, 2020 Outlook is Bright

- Written by: James Skinner

-

Image © Adobe Images

- INR poised for gains Vs USD, GBP in weeks ahead.

- Inflation may have stopped RBI in rate cutting tracks.

- Indian stock market gains also supporting the INR.

- Steady hands at RBI and Fed boost INR attractiveness.

- Yields, weak USD could make INR 2020's 'carry' king.

- Morgan Stanley and CIBC tip INR gains for next year.

India's Rupee has held its own against the Dollar and Pound Sterling this week but is likely to make further gains into year-end and beyond because domestic as well as international factors are tipped to lift the emerging market currency.

Official figures revealed last week a surprise increase in inflation for October, with some measures hitting their highest levels in more than a year.

The Indian consumer price index rose from 4% to 4.6% in October, taking it over the '4% plus-or-minus 2%' Reserve Bank of India (RBI) target, after a sharp increase in food prices that month.

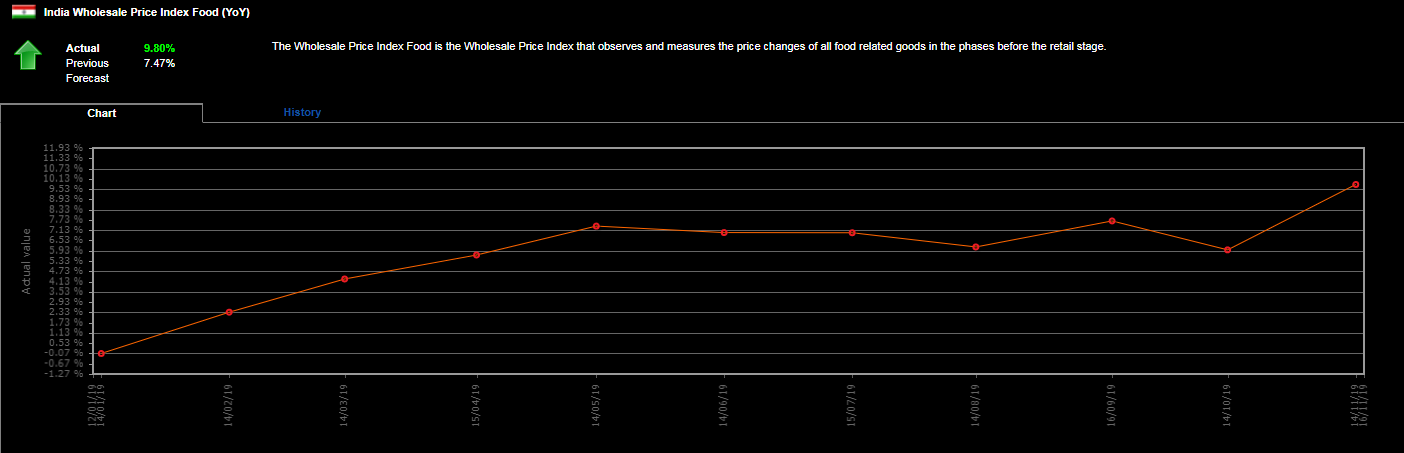

The headline consumer price index is now at 16-month high after food prices paid by consumers increased 7.8% last month, although there could be larger increases than that in store on the road ahead because the wholesale price index rose 9.8% last month.

Above: Indian wholesale price index for food. Source: Netdania Markets.

"We continue to believe that food prices have done sufficient damage to force the RBI to pause its aggressive easing streak at its meeting in December," says Freya Beamish, chief Asia economist at Pantheon Macroeconomics. "It would take a lot of rhetorical wizardry for members to justify a sixth straight cut...Governor Shaktikanta Das has tied his own hands by inadvertently making the 4% inflation target a red line for further easing,"

Beamish tips further increases in Indian foods prices up ahead because "spot prices" for some items are pointing toward gains that could send the consumer price index above the 5% threshold next month, according to her calculations. That, and the earlier data, are problematic for a Reserve Bank of India that has cut its interest rate five times this year, with all cuts coming under new governor Shaktikanta Das, a former government official who took over the RBI after the surprise resignation of Urjit Patel.

The RBI has thrown inflation concerns to the wind this year in its effort to support a slowing economy, which has been beset by structural problems of its own as well as a litany of international risks. Efforts at cleaning up a banking system awash with bad loans, fending off the inflationary threat of rising oil prices and the disinflationary danger that is the U.S.-China trade war all contributed to then-governor Patel's decision to raise rates twice in 2018.

Above: USD/INR rate shown at 4-hour intervals alongside NIFTY index of Indian bluechip stocks.

Changes in interest rates are normally only made in relation to expected movements in inflation but can have a significant influence over international capital flows as well as speculative short-term trading activity. Capital flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency. Rising rates have the opposite effect.

The RBI's rate cuts have left India's 'repo rate' at 5.15%, its lowest in nearly ten years, and have helped to undermine the Rupee which has fallen more than 3% against the Dollar this year and nearly 5% against Pound Sterling. However, rising inflation pressures mean that more rate cuts would be difficult for the RBI to justify in the eyes of the market. That might mean Indian interest rates have gone about as low as they're likely to.

Hopes of a bottom in Indian interest rates, not to mention a robust stock market that is being fueled by both tax cuts and-now the prospect of higher inflation, have helped stabilise the Rupee in the last few weeks. And some say that's likely to remain the case up ahead, which a prediction that's given credence by the correlation between the Rupee and Indian government bond yields. Those yields are stabilising and might even rise slightly if the RBI confirms in December that its rate cutting cycle is over.

Above: Pound-to-Rupee (daily intervals) has negative relationship with Indian 2-year Gov bond yield (orange line, left axis).

"Though the INR was an underperformer within Asia through 2019, we still envisage a recovery in 2020. Stabilization of bond yields will help to counter risks and a 7-year yield of 6.5% is still hard to ignore for investors searching for higher yield," says Bipan Rai, head of FX strategy at CIBC Capital Markets.

Rai and the CIBC team say the Rupee could end the year at 72.0 against the Dollar, a deterioration from Thursday's 71.70, but that it will see out 2019 at 88.61 against the Pound which indicates an anticipated increase over the British currency. However, the Canada-headquartered global investment bank says tips a role reversal for 2020 when the bank see the USD/INR rate falling to 70.30 and the Pound-to-Rupee rate rising to 95.70 by year-end.

"With a stronger EUR, EM currencies that are linked to the stronger EUR performance should do well," says Hans Redeker, head of FX strategy at Morgan Stanley. "We like INR in particular as we believe that growth will pick up and potential equity and bond inflows could push INR stronger."

Above: USD/INR rate (daily intervals) has negative relationship with Indian 2-year Gov bond yield (orange line, left axis).

U.S. investment banking titan Morgan Stanley also tips a solid performance from the Rupee next year. It says the Indian currency offers investors the highest returns after adjusting for volatility in exchange rates - a key concern for so-called 'carry' traders who borrow currencies with low interest rates in order to buy others that have higher rates. Carry traders earn the difference between the two interest rates involved although face an ever-present risk of seeing returns wiped out by swings in exchange rates.

India's attractiveness as a prospect for yield-hungry investors is enhanced by the fact the Federal Reserve (Fed) has recently cut its interest rate three times and signalled that it will now sit on its hands for a while before doing anything else. And if those rates go anywhere in the year ahead, it's most likely to be lower because the only analysts who forecast any changes in rates whatsoever are looking for them to be cut from current levels. That would further enhance the attractiveness of Indian assets.

Morgan Stanley tips the USD/INR rate to see out the current year at 70.50 before it declines to a low of 68.50 by the end of June 2020, only to rise back to 70.50 by year-end. The Pound-to-Rupee rate is seen falling to 92.14 by the end of 2019 before rising to 95.74 before the curtain closes on 2020.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of a foreign exchange specialist. A specialist payments provider can deliver you an exchange rate closer to the real market rate than your bank would, thereby saving you substantial quantities of currency. Find out more here. * Advertisement