The British Pound's Outlook Not Data Dependent

- Written by: Gary Howes

-

Bank of America Merrill Lynch point out that the GBP is no longer responsive to domestic data. So then, what does matter for the British pound’s outlook?

In a startling observation analysts at Bank of America Merrill Lynch have pointed out that UK data is no longer having a meaningful impact on the British pound.

The assumption that the monthly economic data docket has a fundamental bearing on the direction of a currency is a central one to foreign exchange coverage.

What is apparent though is that the influence of data is in constant flux.

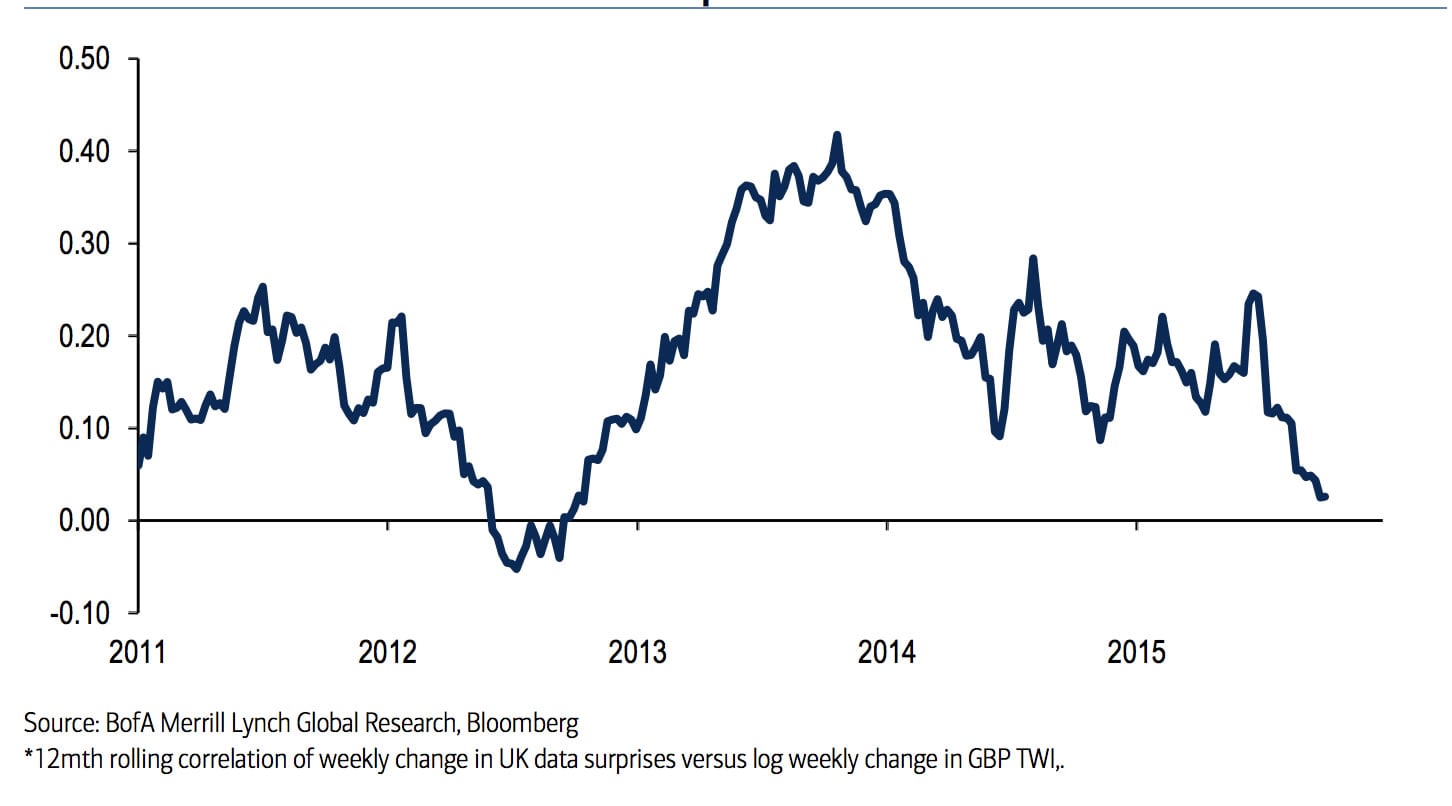

The break-down in the correlation between the pound and UK data is shown in the following chart that represents the 12-month correlation between weekly log changes in the GBP TWI versus the weekly change in UK data surprises:

"GBP TWI has obviously become less correlated to UK data surprises in recent months and that this decoupling accelerated in recent weeks," says Kamal Sharma at BofA Merrill Lynch, "the peak in the correlation coincides with the point at which the fortunes of GBP started to turn during the middle of 3Q."

BofA Merrill Lynch cite price action following the weakest UK service sector PMI since 2012 as being very telling.

"Following that reading, GBP traded broadly higher despite the initial knee-jerk sell-off and even managed to brush aside a more dovish tone to the Bank of England Minutes later in the week," says Sharma.

The GBP sell-off following the release of CPI data was, Bank of America’s view, more a function of renewed market volatility than it was in reaction to the data.

Indeed, short-sterling interest rate futures were only 1-2 ticks higher on the day.

"To us, this would suggest that for now, the market has little interest in trading GBP on a policy divergence basis, particularly with the UK rates market pushing back the timing of the first UK rate hike well into 2016," says Sharma.

It is argued that only when currency markets are more clear on the Federal Reserve’s prospects of tightening interest rates will markets become more interested in trading the pound on policy divergence themes.

We would suggest that this observation could also be read as the British pound will only start rallying once markets are confident that a date for an interest rate rise is solidifying.

Get Ready to Sell the Euro to Pound Exchange Rate

In anticipation of a return of sterling strength Sharma says levels in EUR/GBP are looking increasingly attractive to establish medium-term shorts based on our policy divergence framework and given relatively light positioning in the pair.

“We would look to express this view via options strategies rather through spot as the path toward our year-end forecast of 0.71 is unlikely to be a straight one. Our European economists still look for action by the ECB before the end of the year and, in our view, the UK rates market has pushed back rate hikes too far into 2016 than UK domestic fundamentals would justify,” says Sharma.