Pound Sterling to Rise against Euro and Dollar on a "Hawkish Cut" - Analysts

- Written by: Gary Howes

-

Above: File image of Governor of the Bank of England Andrew Bailey. Image: IMF Photo/Cory Hancock. Licensing: CC 2.0.

The Bank of England preview: downside and upside scenarios for the British Pound.

A note from Barclays says, "A hawkish cut by the MPC is an opportunity for the pound," ahead of the Bank of England's eagerly anticipated August 01 policy decision.

Economists at Barclays expect the Bank of England to pull the trigger on the cutting cycle this Thursday, based on "the revealed preference in June by the core of the MPC to start easing soon."

The rule of thumb is that a rate cut can weigh on the Pound. Indeed, we have seen the UK currency come under pressure over the past five days as market expectations for a cut have gradually inched higher to stand close to 60% at the time of writing.

In theory, a cut would require the difference (approx. 40%) to be priced into the Pound, which would mechanically trigger further downside.

"One risk that could also slow the pace of further GBP appreciation is BoE policy," says Joshua Wilcock, FX Strategist at BNP Paribas. "An August move could precipitate some near-term GBP weakness as rate differentials could narrow given that the market has not fully priced in a 25bp cut at the time of writing."

But the extent of this downside, and whether the currency can ultimately rebound, will depend on the accompanying communication.

A plurality of economists expect an August 01 start date, particularly given the odds of a September cut at the Federal Reserve are now close to 100%, offering the much-desired cover Governor Bailey and his team would prefer.

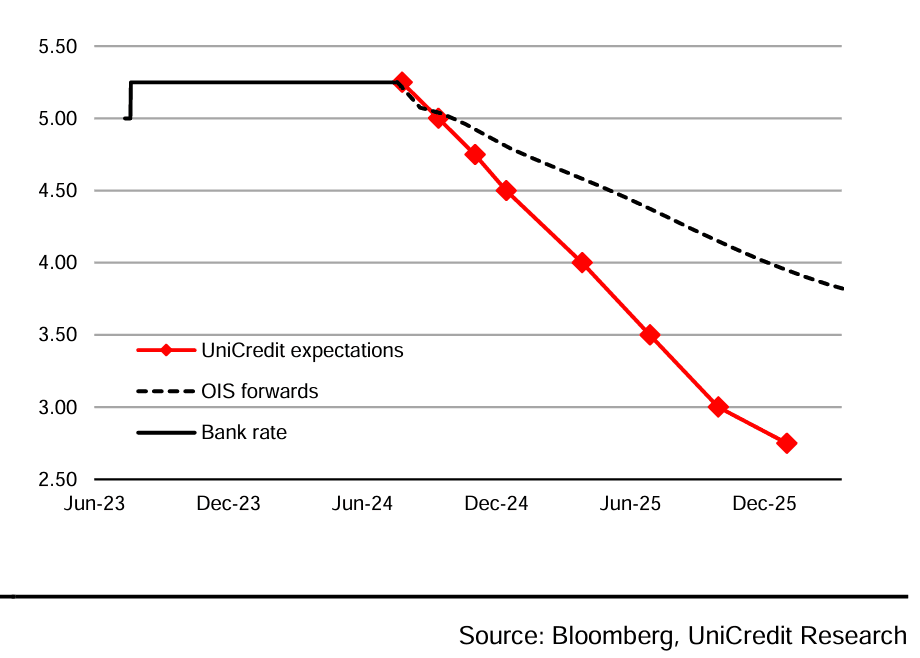

Above: UniCredit thinks the Bank's pace of rate cuts will be faster than the market thinks, saying this can weigh heavily on GBP.

Based on previous voting patterns and subsequent speeches we know two members of the MPC are very unlikely to vote for a cut as soon as August. On the other hand, we have two that are almost certainly to repeat their previous votes for a cut.

This leaves a rump of centrists, including the Governor, his deputy, and the Chief Economist, who will sway the outcome.

Unfortunately, we have heard nothing from these individuals for some time now owing to the pre-election purdah period that forces civil servants into a communications blackout. Analaysts at Oxford Economics say this alone is enough to ensure the Bank delays a cut until September.

GBP: The Downside Case

But, a delayed cut could still result in a softer Pound if it is accompanied by clear guidance that a September rate cut is coming, meaning Pound Sterling could find itself in a lose-lose situation where it falls regardless of the decision.

What ultimately matters is the guidance and how it gels with the forecasts: what do we learn about the prospect for cuts beyond September? After all, the question markets are interested in is the quantum of rate cuts that are to come, not necessarily the start date.

A shallow rate cut profile would likely support the Pound, but a deep profile would result in selling pressures.

📈 Quarter 2 Investment Bank Forecasts for GBP vs. EUR. See the Mean, Highest and Lowest Targets for the Coming Months. Find Out More.

"We now expect the MPC to start cutting rates in September, but we continue to expect a total of 75bp of cuts this year, and a huge 175bp of cuts next year. This is a faster and deeper rate cutting cycle than financial markets expect," says Daniel Vernazza, Chief International Economist at UniCredit.

Any commitment to a steady pace of cuts could spell the end of the Pound's 2024 outperformance.

"We think that the outlook for sterling remains bearish, especially moving into 2025," says UniCredit's Mialich. "Given the intense easing we expect from the BoE. This will likely drag GBP-USD down towards 1.20 and push EUR-GBP back above 0.90 by the end of 2025."

GBP: The Upside Case

If the Bank is non-commital about further rate cuts beyond September, the Pound could soon recover post-decision losses and rise through the summer. Some analysts say this is a likely path to take and would mirror that of a highly data-dependent strategy at the European Central Bank.

"A hawkish cut by the MPC is an opportunity for the pound," says a note from Barclays.

"Rate differentials should not be much affected by the reallocation of cuts across the cycle, implying limited damage for the pound. Instead, demand resilience and a willingness to re-engage with the EU are far bigger positive influences for the pound, in our view, and we look to re-engage on the long side on any further weakness," adds Barclays.

Currency strategists at BNP Paribas say as long as the BoE pursues policy easing in a cautious manner, we would not view this as a reason to stop expecting GBP outperformance over the medium term.

The French bank forecasts the Pound to Euro exchange rate at 1.2050 by year-end and the Pound to Dollar rate at 1.28.