Pound Sterling Rises against Euro and Dollar on "Less Bad" PMI and Labour Market Stats

- Written by: Gary Howes

Image © Adobe Stock

Pound Sterling has risen from recent lows against the Euro and extended a recovery against the Dollar following the release of some relatively supportive UK economic data.

UK labour market figures came in better than expected when released at 07:00 on Tuesday, this was then followed by the UK PMI survey for October at 09:30, where a welcome improvement was recorded in the manufacturing sector.

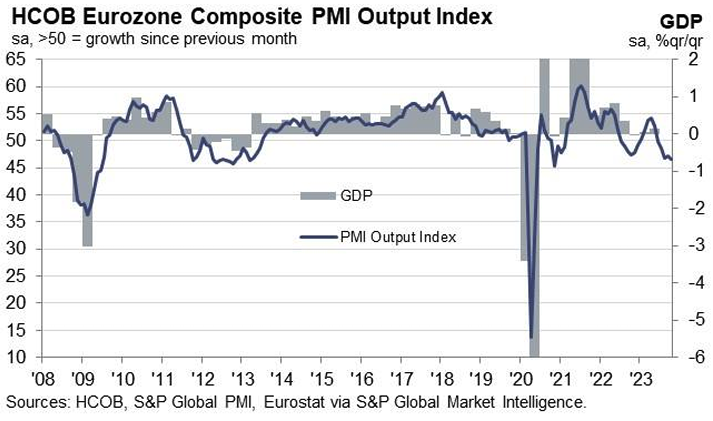

From a pure FX perspective, the UK PMIs were more constructive than those published by the Eurozone just thirty minutes earlier, where a downturn in activity accelerated.

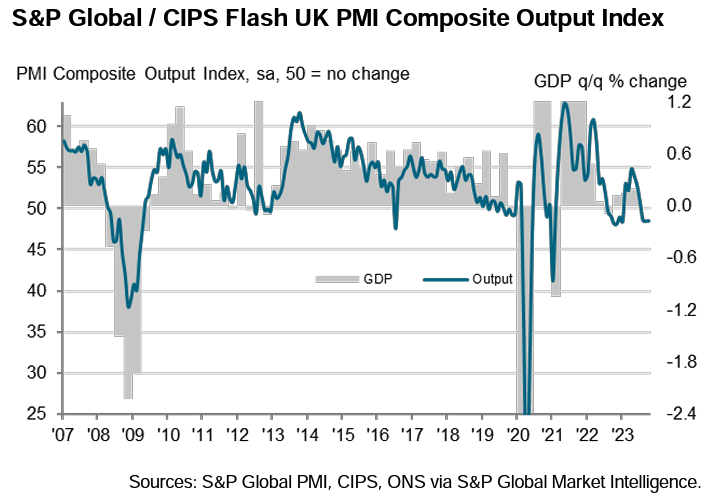

The UK's manufacturing PMI read at 45.2 in October, which is ahead of the 44.7 the market was anticipating and up on September's 44.3. The service PMI read at 49.2, which is a touch lower on September's 49.3 and the consensus expectation of 49.3.

The composite figure - which balances the findings to give a weighting that represents the broader economy - read at 48.6, slightly below the expected 48.7 and up on September's 48.5.

"The UK economy continued to skirt with recession in October, as the increased cost of living, higher interest rates and falling exports were widely blamed on a third month of falling output," says Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

The data is consistent with a slowing economy, but from a currency angle, the miss on expectations was relatively negligible. And as mentioned already, the Eurozone's October PMI report was significantly worse.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

The Pound to Euro exchange rate is quoted 0.40% higher at 1.1511, the Pound to Dollar exchange rate is at its highest level in a week at 1.2260.

"While the PMI survey also signals weakness for the UK economy, the results are somewhat less dire than on the continent," says Salomon Fiedler, an economist at Berenberg Bank.

The British Pound had edged higher ahead of the PMI release following some better-than-expected labour market figures. The ONS released its delayed labour market survey, which showed the unemployment rate fell to 4.2% in August, defying expectations for an unchanged reading of 4.3%.

The situation was aided by a smaller-than-expected loss of jobs at -82K on a rolling three-month basis in August (vs. -198K expected and a material improvement on July's -207K).

The ONS warns of elevated uncertainty when measuring the labour market as it alters methodology to ensure greater accuracy, and revisions to today's data over coming weeks are therefore likely.

On the margin, these data suggest the labour market is not deteriorating as fast as the Bank of England might have liked; therefore, it raises the prospects of a final 25 basis point hike in either November or December.

This is supportive of the Pound and could underpin the currency near current levels.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

"Looking at the 'experimental' data, we can see that unemployment in the UK is remaining stable, for now," says Marcus Brookes, chief investment officer at Quilter Investors. "We know that economic growth in the UK is slowing and could potentially turn negative for the fourth quarter, so today’s data provides further evidence that things may be beginning to roll over. For the Bank of England this may be just enough to continue with a pause at its next interest rate decision.

Even though the headline numbers beat expectations, the UK labour market does continue to 'loosen' with job vacancies in the July to September period at 988K, down 43K on the April to June period. This makes for a 15th consecutive quarter of falling vacancies.

This can keep a lid on any enthusiasm in the market for materially jacking up expectations for further rate hikes, thereby limiting the Pound's upside potential.

Looking ahead, a services PMI of 49.5 is expected from the UK in the 09:30 BST release, with the manufacturing PMI anticipated at 44.6. The rule of thumb is that the Pound will move according to whichever side of expectation the data lands: higher on a beat, lower on a miss.

"If the forward-looking balances in recent activity surveys are anything to go by, October's flash S&P Global/CIPS PMI surveys are likely to signal a further contraction in private sector output," says Andrew Goodwin, Chief UK Economist at Oxford Economics.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes