Pound Sterling's "Awful August" is Over, But the Rout Might Continue

- Written by: Gary Howes

Image © Gov.uk. Picture by Simon Dawson / No 10 Downing Street.

August saw the British Pound suffer its worst monthly performance against the Dollar since the fallout from the Brexit referendum of 2016 as a consequence of extreme negative investor sentiment towards the UK, something the new Prime Minister must address.

"Britain’s political and economic houses in disarray have taken a heavy toll on the pound, suggesting further declines ahead despite next week’s leadership change on Sept 5," says Joe Manimbo, Senior Market Analyst at Convera.

The Pound to Dollar exchange rate (GBP/USD) fell 4.67% in August; only October 2016 saw a bigger decline with a 5.68% slump as investors abandoned UK assets in the wake of the Brexit referendum result.

The Pound to Euro exchange rate (GBP/EUR) meanwhile endured its worst month in over two years, with August's 2.57% decline only beaten by that of May 2020 (-3.28%), which came at the height of Coronavirus panic.

There are numerous factors behind the Pound's ongoing decline, none of which look set to ease, or reverse near-term.

For GBP/EUR, renewed downside comes amidst falling natural gas prices in the Eurozone and the UK. We have reported at length on Pound Sterling Live that the Euro suffered when gas prices were surging, it therefore stands it would benefit when they are falling.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes

Currency markets are meanwhile prepared for a 75 basis point hike out of the European Central Bank (ECB) in September, this would be a statement of intent by the ECB that it intends to get on top of inflation expectations.

The Bank of England is meanwhile also expected to hike in September, but by a smaller 50 basis points. The currency market has nevertheless decided to ignore UK rate hike expectations, which is obvious when we observe how UK gilt yields of shot higher but the currency continues to decline.

In the past rising bond yields reflected expectations for higher Bank of England interest rates, which in turn supported Sterling.

But now global investors are unwilling to buy UK assets, perhaps as they fear the UK government's ability to repay that debt and also partly because investors don't tend to buy such assets at times of dour global economic sentiment.

"The rout in UK assets may not be over as Britain grapples with a toxic mix of double-digit inflation and a looming recession. Meanwhile, the weaker pound and higher commodity prices are eating into the UK’s terms of trade, which has correlated with the slide in GBP/USD this year," says analyst George Vessey at Western Union Business Solutions.

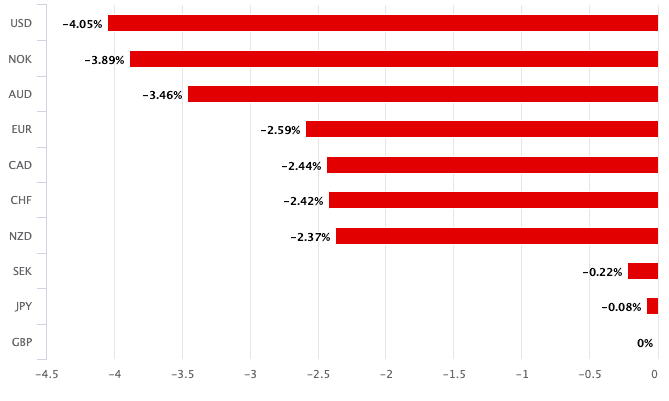

Above: GBP performance in August.

Global investor sentiment in September will be key in determining whether the Pound can pick itself up from the floorboards.

Stock markets have faltered as investors fear further U.S. Federal Reserve interest rate hikes over coming months, which will push higher the cost of finance, not just in the U.S. but across the world.

This signals slowing global growth, which tends to benefit the U.S. Dollar and penalise 'risky' assets such as equities.

The Pound is a 'high beta' currency in that it tends to rise when global markets are rising and fall when the opposite is true.

Therefore, the current environment is unhelpful and as long as stocks continue to fall expect the UK currency to follow suit.

* Speak to a money transfer expert about the outlook and implications for your payments. Horizon Currency are here to help, they are one of the remaining payment providers that offers one-on-one service, while still delivering bank-beating exchange rates (3-5% more FX than the bank), please get in touch here. *Advertisement.

From a fundamental perspective the UK is an importing nation that does not export goods or commodities. Think of how the likes of Canada and Australia have seen their currencies benefit since Russia's invasion of Ukraine: these are commodity rich countries that see their export earnings rise as commodity prices rise.

The boost to commodity exports and their mineral and energy wealth has boosted their terms of trade.

The UK, on the other hand, is a net importer of commodities and goods.

Therefore the Pound cannot rely on UK exports to keep it propped up. This means the Pound is on a multi-decade trend of depreciation:

Above: The GBP/USD post-Bretton Woods, showing a long-term trend of depreciation. Set your FX rate alert here in order to stay on top of the market.

It would take years for the UK economy to change in a manner that its terms of trade fundamentally improved and started to benefit the Pound.

This is of course not guranteed, given the country's political composition (successive Labour and Conservative governments have contributed to the trends that leave the economy where it is).

Therefore, those holding Sterling should be aware that they are likely to see their global purchasing power whither over coming years.

Near-term, much could depend on the incoming Prime Minister, who is to take the reins next week.

In all likelihood it will be Liz Truss, who will be expected to immediately address the cost of living crisis.

An effective response by the new Prime Minister could make a significant dent in both realised inflation levels and broader consumer and business confidence in the UK.

This could ease downside pressure on the British Pound.

It is widely reported Truss is preparing to fast-track an emergency spending package to help people cope with surging energy costs.

The report says Truss could announce the measures before Parliament rises on September 22 for a recess when political parties hold their annual conferences.

Truss is apparently "eager to act as soon as possible" on energy bills.

For the Pound, anything that can nip the inflation surge and restore consumer confidence would be supportive and could ultimately preserve it from any major losses over coming weeks and months.

However, the cost will be huge and risks bloating the UK's debt burden to the extent international investors are less willing to invest in Sterling assets.

Compare Currency Exchange Rates

Find out how much you could save on your international transfer

Estimated saving compared to high street banks:

£2,500.00

Free • No obligation • Takes 2 minutes