Norwegian Krone Takes Norges Bank Outlook in Stride, but Upside Ahead

- Written by: James Skinner

-

Image © Norges Bank

- GBP/NOK spot rate at time of writing: 11.76

- Bank transfer rate (indicative guide): 11.35-11.43

- FX specialist providers (indicative guide): 11.58-11.68

- More information on FX specialist rates here

- Set an exchange rate alert, here

The Norwegian Krone was a middle of the road performer among major currencies on Thursday, enabling GBP/NOK to arrest an earlier decline as the Nordic currency took in its stride suggestions from the Norges Bank that it could begin lifting interest rates before the year is out.

Norway's Krone remained a contender for the top spot among major currencies in 2021 but was lower against many counterparts following the Norges Bank's March monetary policy decision.

The Pound, U.S. Dollar, Canadian Dollar and non-oil commodity currencies all rose against the Krone this Thursday.

“When there are clear signs that economic conditions are normalising, it will again be appropriate to raise the policy rate,” says Governor Øystein Olsen.

The cash rate remained at 0% and the midpoint between an overnight lending rate of 1% and a commercial bank deposit rate of -1%, with policymakers citing a recovery "held back by higher infection rates and strict containment measures," for overlooking above-target inflation.

"They are keeping the door open for September. Today’s path is broadly in line with what markets have been pricing," says Kjetel Olsen, chief economist at Nordea Markets. "We could see Norges Bank signalling a first rate hike in September at their June meeting."

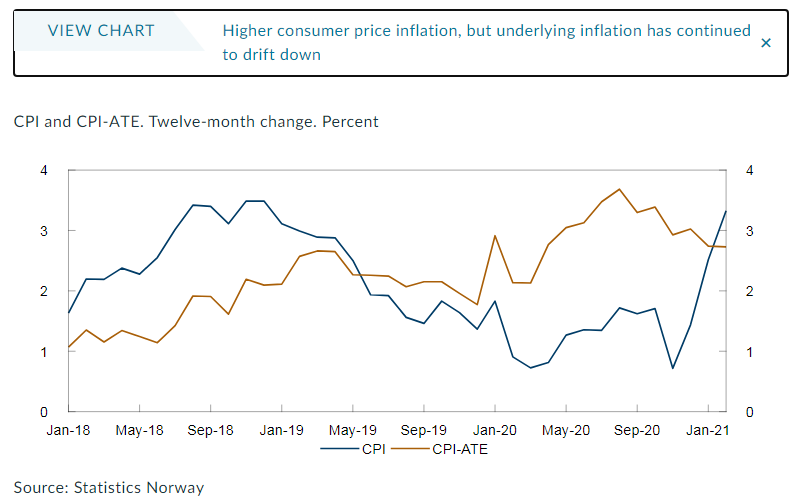

Norwegian inflation rose above the 2% target in January and reached 3.3% last month, although Olsen and colleagues noted this week that lacklustre wage growth and an often-rampantly strong Krone will counter this inflation and spare the economy from any interest rate rises for the time being.

But higher borrowing costs are likely to be seen before long after the bank said Thursday "the policy rate will most likely be raised in the latter half of 2021," bringing forward from 2022 the projected date of lift-off. The "latter half" could refer to either September or December's decision.

"We think it will raise interest rates sooner and faster than it currently projects," says David Oxley at Capital Economics. "Norwegian GDP is already closer to its pre-virus level than most. Moreover, the run-up in oil prices will also help to support mainland activity this year. We recently raised our oil price forecasts and now expect Brent to peak at $80 per barrel in Q3, from $68 currently. Against this backdrop, while policymakers do not seem unduly worried about inflation prospects, we suspect that domestic price pressures and the core inflation rate will pick up again during the second half of the year."

The difference between Thursday's and the previous projection is small, and likewise with the new projection and financial market pricing, so may explain why the Krone took the statement in its stride rather than as cause for celebration. But if Capital Economics is right in its expectations, the Norwegian Krone could find its feet again before long.

The prospect of Norway becoming the first major economy to embark on an interest rate hiking cycle, more so one which comes sooner and steeper than markets anticipate, is a supportive feather in the cap of a currency that also appears to be viewed in Oslo as ancillary aid in the inflation-targeting toolbox.

"There are some signs of higher cost growth both globally and in Norway, but the krone appreciation and prospects for moderate wage growth suggest that inflation will move down ahead," the Bank said Thursday. "The Committee also placed weight on the marked rise in house prices since spring 2020."

Exchange rates including those of Norway tend to rise in response to expectations of higher interest rates but in the process stronger currencies act to reduce the cost of imported goods and services, which means they can act to reduce inflation without the need for a central bank to lift borrowing costs.

Interest rate changes and tools like quantitative easing are generally preferred by central bankers for controlling inflation but as has been demonstrated by frequently voiced European Central Bank (ECB) concerns about strength in the Euro; currency moves are far from being insignificant factors.

"The Committee is still concerned that house prices have risen markedly since spring," says Oddmund Berg, a macro economist at DNB Markets. "The rate path has the policy rate lifted in the second half of 2021, gradually increasing to 0.75% in Q4 2022. The new path reaches a top of 1.36% in Q4 2024."

Norway's Krone can only delay interest rate rises for so long however, and partly due to the trajectory of prices in the housing market, which is less readily influenced by exchange rates. "A long period of low interest rates increases the risk of a build-up of financial imbalances," Norges Bank said Thursday.

"Norges Bank shows itself to be the hawkish outlier in an otherwise cautious central bank arena. And it's cemented the NOK's rather attractive position within the G10 FX space. The break below the EUR/NOK 10.00 level seems only a matter of time," says Petr Krpata, chief EMEA strategist for FX and rates at ING. "NOK should benefit from the constructive outlook on the oil prices this year as well as the expected recovery of the eurozone and Norwegian economies from Q2 onwards. As a currency with one of the highest betas in G10 FX, the expected friendly risk environment should help facilitate NOK upside."

The Krone has been vying with Sterling and the Canadian Dollar for top spot in the league table in 2021 but over a longer one-year lookback window the Nordic unit has been the winner by a country mile.

USD/NOK had fallen -1.57% during the 2021 year-to-date on Thursday, less than the -2.4% fall in USD/CAD or the 2.2% increase seen in GBP/USD. However, USD/NOK remained -25% lower over a one-year lookback, reflecting far larger gains for the Krone than were seen by either Sterling or the Loonie.

Thursday's GBP/NOK rate of 11.77 was -8.9% over a one-year lookback while the Euro-Krone of 10.06 was -3.4% for 2021 and -17.5% over 12 months.