Swiss Franc Still a Safe Haven but Could Struggle Up Ahead, Says Barclays

"In this sense, Switzerland is already an exception in light of its very small stock of government debt and international ownership. Instead, the 'safe asset' that Switzerland exports to the world is Swiss franc-denominated deposits" - Barclays.

Image © Adobe Stock

The Swiss Franc remained one of the top-performing major currencies of the period in the fading light of March and will still retain its appeal as a financial safe haven even as it struggles to advance any further against the Pound, Euro and others through the rest of the year, according to Barclays Research.

Switzerland's Franc rose against all major counterparts in the G10 basket on Thursday while also climbing in relation to most of the broader G20 grouping as stocks and bonds notched up gains in many parts of the world and a recent downdrift in U.S. Dollar exchange rates deepened.

Similar is true of the performance for March with the Swiss currency having given ground to only the Japanese Yen and Pound Sterling even after financial stability risks emanating from the U.S. banking sector led the federal government to force a merger between Credit Suisse and UBS.

"In all, the de-classification of the Swiss franc from 'safe-haven' status requires radical shifts in the structure of Switzerland's balance sheet via sizeable 'safe asset' outflows," says Lefteris Farmakis, an FX strategist at Barclays.

"This is very unlikely to materialise in the near term on the back of the Swiss banking sector turmoil, and it is also debatable whether this shift may unfold over the longer term," Farmakis writes in a late March research briefing.

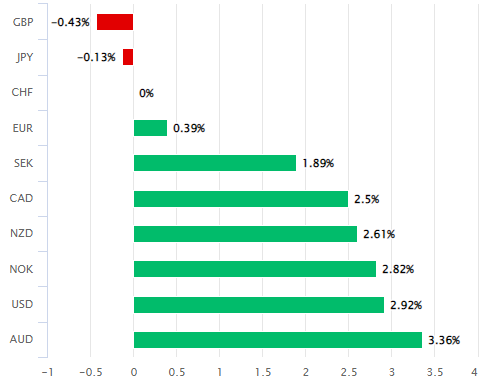

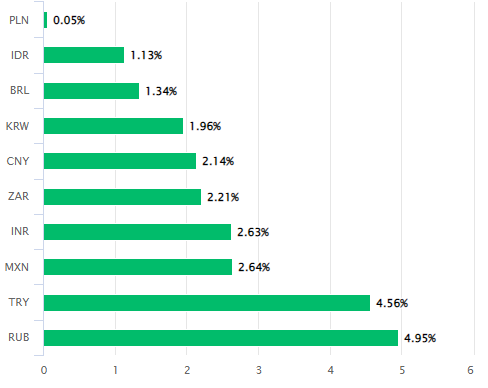

Above: Swiss Franc performance in March relative to G10 and G20 currencies. Source: Pound Sterling Live.

The mid-month rout in Credit Suisse equity and debt securities reflected "a loss of confidence" in the institution, according to the Swiss National Bank (SNB), connected with shrinking revenues and large but one-off accounting charges that led costs to balloon to 117% income this last financial year.

Hence how speculation about the feasibility of efforts to turnaround Credit Suisse was able to proliferate in the wake of this month's small bank failures in the U.S., while ultimately leading to the forced merger with UBS and questions in the market of whether the Swiss Franc's safe-haven appeal is at risk.

"It may therefore come as a surprise that there is no precise 'definition' of a 'safe currency' nor a set of all-encompassing criteria that facilitate a definitive answer to this question," Farmakis says.

"That said, an understanding of the main features underpinning a 'safe haven' currency and how much scope there is for a regime shift can take us some way towards answering this question," he adds.

Farmakis and colleagues say a country's ability to issue what the market perceives as "safe assets" is a crucial feature and determinant of a currency's appeal to investors as a so-called safe-haven, and on this metric at least, the Swiss Franc still has very few comparable rivals.

Source: Barclays Research. To optimise the timing of international payments you could consider setting a free FX rate alert here

Source: Barclays Research. To optimise the timing of international payments you could consider setting a free FX rate alert here

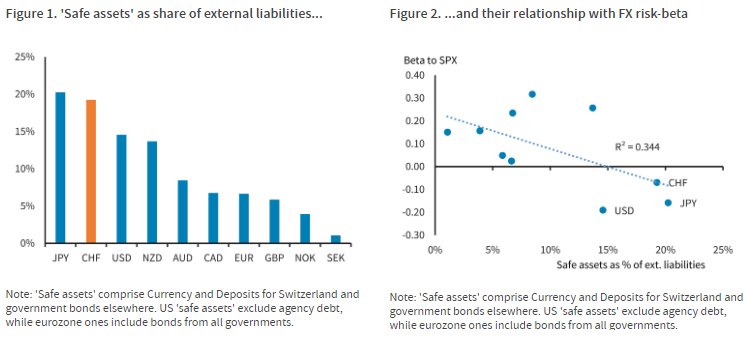

"Figure 1 shows thus-defined 'safe assets' across the G10 as a share of external liabilities. The three G10 currencies typically ascribed 'safe haven' status (JPY, CHF and the USD) top the list, with the US share likely under-estimated as agency debt is excluded from 'safe assets' due to lack of data," Farmakis says..

"What is more, there is a fairly strong linear relationship between the share of 'safe assets' in external liabilities and the risk-beta of each currency. The latter is calculated via a regression of monthly changes in FX TWI on such changes in the S&P 500 index since 2000," he adds.

So-called safe assets are generally taken to be government bonds or equivalent instruments issued in the relevant currency, although the safe-haven currencies tend to be those countries where "safe assets" pay comparatively low levels of interest but are large in their volume of issuance.

Put differently, the safe haven currencies tend to be those of countries where the cost of government debt is low relative to other countries and the supply of government debt is large relative to the debts of the private sector and the debts of other countries.

"In this sense, Switzerland is already an exception in light of its very small stock of government debt and international ownership. Instead, the 'safe asset' that Switzerland exports to the world is Swiss franc-denominated deposits," Farmakis says.

Source: Barclays Research. (If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.)

Source: Barclays Research. (If you are looking to protect or boost your international payment budget you could consider securing today's rate for use in the future, or set an order for your ideal rate when it is achieved, more information can be found here.)

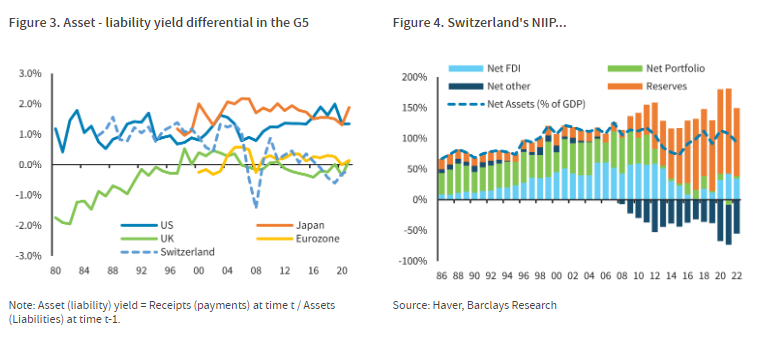

The low interest cost of Switzerland's government debt and its large amount of investments in foreign assets mean the country and currency earn one of the highest yields among sovereigns from the mismatch between foreign assets and liabilities, which is a persistent feature of 'safe haven' currencies.

That is one important feature of the country, economy, and currency that would need to change in order for Switzeraland's safe-haven appeal to be questioned or otherwise jeopardised credibly, and the Barclays Research team sees little chance of this happening anytime soon, if even at all.

"A more difficult question to answer is whether confidence in the Swiss banking system has been eroded to a degree that a slow-burn process may have started, unfolding over several years. Fortunately, this scenario has limited repercussions for the franc over the foreseeable future," Farmakis says.

"On this basis, we expect the franc to remain resilient both versus the euro and, in a EUR recovering environment, also the dollar," he adds, after also citing SNB foreign exchange policy as an additional source of support for the currency.

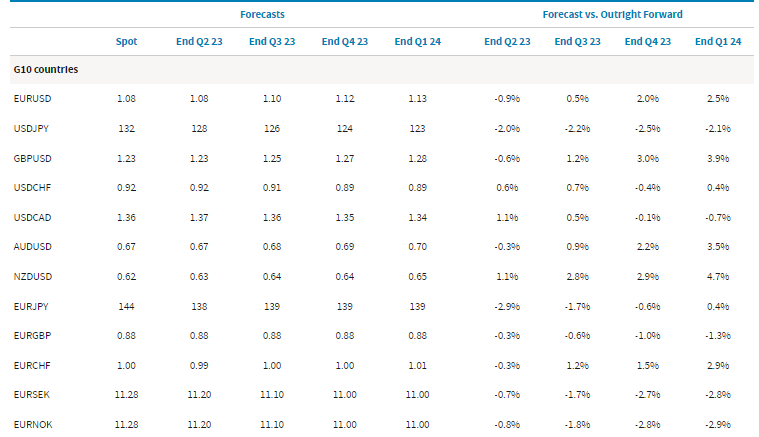

Barclays' forecasts are consistent with recent price action in Swiss exchange rates and suggest the all-important EUR/CHF pair is likely to fluctuate around parity over the course of the year, while GBP/CHF is tipped to spend much of its time in the 1.13 area and USD/CHF is seen dipping from 0.92 to 0.89.

Source: Barclays Research.

Source: Barclays Research.