GBP/NZD Week Ahead Forecast: Sagging into Jackson Hole

Pine timber being exported from Wellington, New Zealand. Photo by James Anderson, World Resources Institute.

The Pound to New Zealand Dollar exchange rate has resumed its recent correction lower in tandem with many US Dollar pairs and it could be likely to remain heavy, with a downside bias over the coming days.

GBP/NZD rallied briefly to 1.15 last week after the Reserve Bank of New Zealand surprised the market by cutting its cash rate but the move was quick to fade, perhaps owing to the bank’s new forecasts.

These suggested as much as 100 basis points of additional cuts are likely over the year to next August when the market had been pricing in a much deeper 200 basis point reduction for that period.

The main Kiwi pair, NZD/USD, has since recovered back above 0.60 as a result, aided by a softer US Dollar, which has led GBP/NZD to recede back below 2.13 despite a buoyant performance from Sterling.

“Our proprietary flows show USD selling across the board so far in August, particularly from hedge funds and corporates. EUR, JPY and GBP have benefited the most, but more recently also high beta G10 currencies and EM FX,” BofA Global Research strategists said in a Monday note to clients.

Above: Pound to New Zealand Dollar rate shown at daily intervals with Fibonacci retracements of June upturn and selected moving averages indicating possible areas of technical support.

“Despite GBP being the weakest in G10 so far in August, our investor proprietary flows remain positive, with hedge funds in particular offering strong support. GBP positioning is long, but not stretched, with hedge funds having more room,” the BofA team also said.

The nascent rebound in NZD/USD is a headwind for the negatively-correlated GBP/NZD pair but the currently buoyant performance from GBP/USD is something that might limit the downside in GBP/NZD this week.

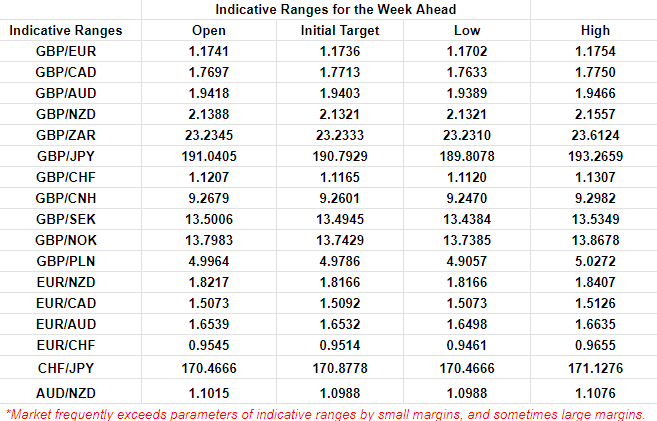

The author’s model suggested earlier on Monday that a relatively narrow range between 2.1321 and 2.1557 was likely for the week ahead and while GBP/NZD has since slipped through the bottom of this, there is some technical support just above the nearby 2.11 handle that might frustrate further losses in the short-term.

“The Kiwi has quickly put last week’s OCR cut and dovish U-turn by the RBNZ behind it and has resumed focussing on global themes. That also makes it a little more sensitive to moves in the USD, which is continuing to track lower as US bond yields fall,” ANZ Research strategists said.

Above: Quantitative model estimates of possible ranges for the week. Source: Pound Sterling Live.

“Falling interest rates were a key factor undermining the Kiwi in the lead-up to last week’s cut, and they’re likely to have a similar impact on the USD as the Fed inches closer to easing. On that score, all eyes are on this week’s Jackson Hole Economic Symposium,” they added in a Monday note to clients.

Much about the near-term trajectory of GBP/NZD is likely to be determined by the direction of the US Dollar before and after the Federal Reserve’s Jackson Hole Symposium on Thursday and Friday, where the main event is a Friday speech from Chairman Jerome Powell.

Market focus will be on whether he validates or pushes back against current expectations for as much as 100 basis points worth of interest rate cuts from the Fed this year, which matters for the US Dollar because this kind of easing would be likely to erode its yield advantage over other currencies.

Any validation of the market’s outlook for US rates would likely act as a headwind for GBP/NZD, though Sterling will also be sensitive to a subsequent speech from Bank of England Governor Andrew Bailey, and particularly any remarks on what last week’s data deluge means for the UK interest rate outlook.

However, before then, GBP/NZD could potentially benefit somewhat on Wednesday and Thursday if Kiwi credit card spending data for July and retail sales figures for the second quarter remain weak, as this would reinforce the case for further interest rate cuts from the Reserve Bank of New Zealand.