GBP/USD Week Ahead Forecast: Bond Markets in Focus

- GBP/USD finds tentative foothold above 1.23 after sell-off

- Scope for support at 1.2346, 1.2288 & 1.22436 short-term

- Attempt at rebound possible if government bonds stabilise

- But U.S. data, uncertainty about debt ceiling deal pose risk

Image © Adobe Images

The Pound to Dollar exchange rate entered the new week near two-month lows but could attempt to pare away some of its recent losses if calm returns to government bond markets on both sides of the Atlantic in the days ahead.

Dollars were bought widely last week, enabling the greenback to strengthen its grip on the top spot in the major currency league table for the month of May while pushing an otherwise resilient Pound back to some of its lowest levels since the opening of April at one stage.

"Cable losses have steadied in the low 1.23 zone and while short-term patterns look soft the pound is finding some support on weakness ahead of the 1.23 line, which has blunted bear pressure," says Shaun Osborne, chief FX strategist at Scotiabank.

"Loss of support at 1.23 targets more losses to the 1.21 area. Above 1.24 in the short run will lift the GBP," Osborne writes in Monday market commentary.

Live GBP/EUR Money Transfer Exchange Rate Checker | ||

Live Market Rate: | get quick quote | |

Corpay: | ||

Banks: Median Low | ||

Banks: Median High | ||

These data are based on the spread surveyed in a recent survey conducted for Pound Sterling Live by The Money Cloud. | ||

Sterling's losses were initially catalysed by a rout in the UK government bond market after April inflation figures led to a significant upward revision to market expectations for the Bank of England (BoE) Bank Rate, although pressure was reinforced on Friday by prices data out in the U.S.

This was after an uptick in the preferred inflation measure of the Federal Reserve (Fed) threw fuel on a global government bond market bonfire that had burned with greater intensity throughout the week but which actually dated back to the May 10 release of the official U.S. inflation measure.

"The USD has lifted in part because market pricing has shifted from rate cuts to rate hikes in mid-2023. Market pricing for the start of rate cuts have been pushed back to match our view of January 2024," says Joseph Capurso, head of international economics at Commonwealth Bank of Australia.

"Still, the USD can lift from an upside surprise to the non-farm payrolls report on Friday. The FOMC will hope growth in average hourly earnings decelerates from too-strong rates despite low unemployment," Capurso and colleagues write in a Monday research briefing.

Above: Quantitative model estimates of ranges for selected pairs this week. Source Pound Sterling Live. Click the image for a more detailed inspection.

Capurso and colleagues said on Monday the Pound-Dollar rate could fall as far as 1.2130 this week if U.S. non-farm payrolls and wage figures out on Friday, or any other data, reinforce the latest upturn in government bond yields and U.S. Dollar exchange rates.

Friday's employment figures are data highlight of what is a quiet week in the UK calendar but Wednesday's Job Openings and Labour Force Turnover Survey (JOLTS) and Thursday's Institute for Supply Management (ISM) Manufacturing PMI survey could also impact the Dollar and bond markets.

"Evidence of sharper slowdown in employment growth would dampen speculation over further Fed rate hikes and encourage expectations for rate cuts later this year," writes Lee Hardman, a senior currency analyst at MUFG, in a Friday research briefing.

"Similar to in February, we are not expecting this move higher in US yields and the USD to be sustained. With US growth and inflation set to slow further and rates already at more restrictive levels at close to 5.00%, the balance of risks is titled to the downside for yields," Hardman adds.

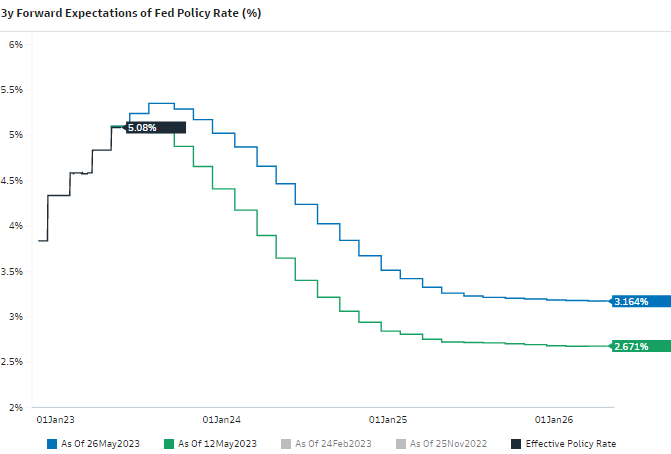

Above: Changes in market-implied expectations for Federal Reserve interest rate. Source: Goldman Sachs Marquee. Click the image for a more detailed inspection.

Meanwhile, the Pound to Dollar rate could benefit if a weekend agreement between the White House and Republican Party's Congressional leadership gains sufficient support in both houses of Congress in order to raise the government debt ceiling in time to avert a technical default.

Political differences over government spending plans had led many to speculate in recent weeks that an agreement on the budget and borrowing limit would not be reached before the U.S. Treasury runs out of cash on the estimated x-date of June 05.

"It’s equivalent to a bit more than a quarter-point rate hike in terms of its drag on growth," says Avery Shenfeld, chief economist at CIBC Capital Markets, in a Monday reference to the proposed agreement.

"That could take a bit of the pressure off the Fed to hike again, or at least given them room to take a pass on a hike in June and wait until the July meeting to get a better picture on how growth and inflation data are evolving, assuming Friday’s payrolls data aren’t too hot to handle," he adds.

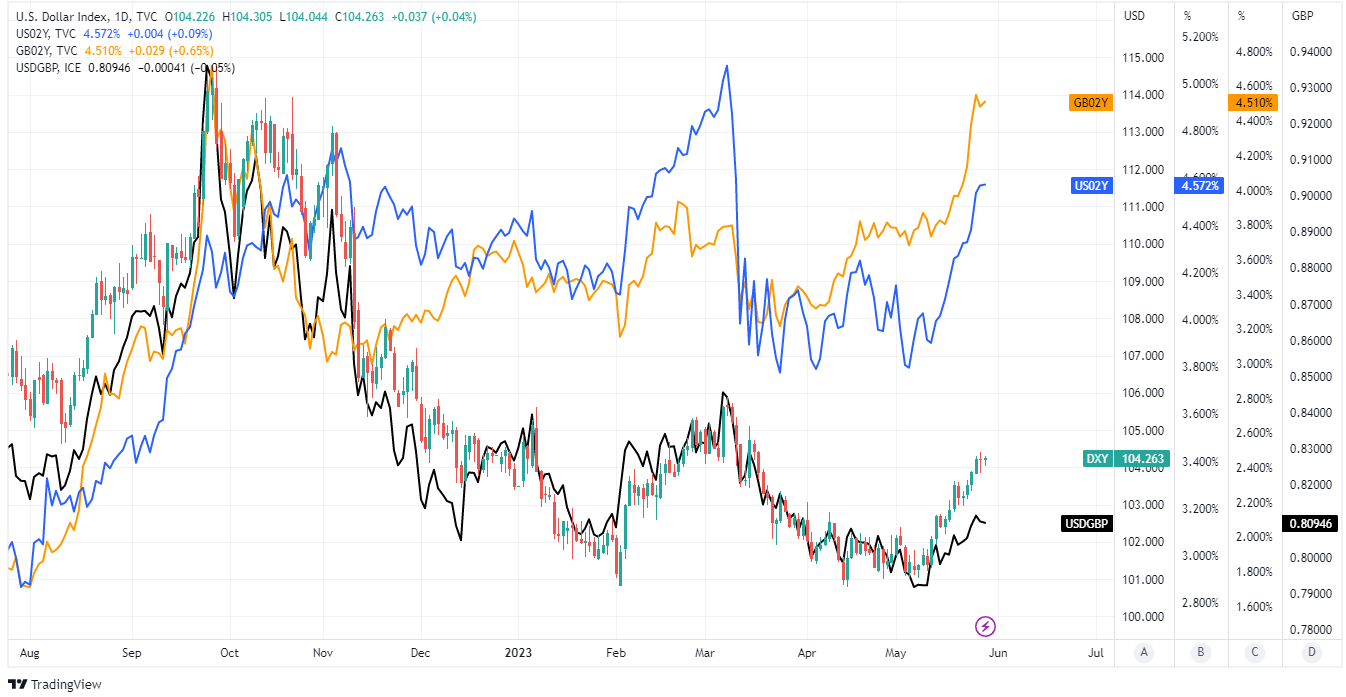

Above: Dollar Index shown at daily intervals alongside 02-year UK and U.S. government bond yields, and USD/GBP. Click for a more detailed inspection.

Above: Dollar Index shown at daily intervals alongside 02-year UK and U.S. government bond yields, and USD/GBP. Click for a more detailed inspection.

Live GBP/EUR Money Transfer Exchange Rate Checker | ||

Live Market Rate: | get quick quote | |

Corpay: | ||

Banks: Median Low | ||

Banks: Median High | ||

These data are based on the spread surveyed in a recent survey conducted for Pound Sterling Live by The Money Cloud. | ||

The bipartisan proposal means less government borrowing and spending than otherwise in the coming years so it's possible that it will keep interest rate expectations from rising much further and enable U.S. Treasury debt issuance to resume without leading upset for the bond market.

To the extent that this is the case, the proposed agreement could further supportive of the Pound to Dollar rate, though this is by no means assured.

"The deal caps federal spending and suspends the debt ceiling until 1 Jan 2025, after the next Federal election," writes Elsa Lignos, global head of FX strategy at RBC Capital Markets, in a Monday market commentary.

"The fiscal impact will be a small drag but note that prior to the deal, the US was the only G10 country with a positive fiscal impulse both this year and next and even after the deal, the US is no outlier in fiscal drag," she adds.