GBP/EUR Rate Week Ahead Forecast: Pushing the Boundaries

- Boundaries of 1.1633 to 1.1662 range could be pushed

- Scope for 55-day average to be stress-tested this week

- Upside could be limited on rebound to or above 1.1675

- Bonds, BoE the highlights of an action-packed calendar

Image © European Commission Audiovisual Services

The Pound to Euro exchange rate remains in the upper quartile of the year’s range but an action-packed economic calendar, bond markets and the Bank of England (BoE) interest rate outlook could see each or all push the boundaries of an anticipated 1.1633 to 1.1662 range for the week ahead.

Pound Sterling rallied from a two-month low against the Euro last week while outperforming all currencies in the G10 grouping except for the Japanese Yen and despite a sparse economic calendar offering up only a downbeat set of S&P Global surveys of manufacturing and services sectors for the market to chew on.

Rising international stock markets, modest increases in government bond yields and sluggish single currency were potentially among the factors driving the Pound to Euro exchange rate higher last week and an exceedingly busy economic calendar over the coming days now comes into focus.

Monday saw the Euro rise against the Pound and other peers after the Eurozone reported above-consensus core CPI inflation prints for July, with the month-on-month change coming in at -0.1%, which was less than the -0.5% the market was looking for.

The year-on-year reading stood at 5.5%, which was above expectations for 5.4% and raises the prospects of a further 25bp hike at the European Central Bank in September in what amounts to a supportive development for the Euro.

The inflation data came alongside Eurozone GDP data which beat expectations at 0.6% year-on-year, suggesting the economy is proving more resilient than many in the market were expecting.

Looking ahead, the Bank of England's Thursday policy update forms the main focus for Sterling. “The Bank of England is expected to raise rates on Thursday by at least 25bps (with markets somewhat priced for a 50bps hike),” writes Thomas Ryan, an economics and markets analyst at Longview Economics, in a research briefing.

The odds are unrewarding for anybody betting that either or all of the above events could lead the boundaries of an anticipated 1.1633 to 1.1662 trading range in the Pound to Euro to stress tested, if not eroded entirely over the coming days.

“We continue to see relative rates as a positive for EUR/GBP, which is one of several reasons behind our fundamental predisposition of buying EUR/GBP dips,” writes Kirstine Kundby-Nielsen, an FX analyst at Danske Bank, in a research briefing.

Above: Pound to Euro rate shown at daily intervals.

“Markets see a near-identical probability of the MPC raising Bank Rate by 25bp and 50bp at next week’s meeting. We’re firmly of the view, however, that the Committee will opt to hike by 25bp, to 5.25%, given the spate of downside data surprises since its last meeting,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

“June CPI inflation matched the MPC’s forecast, while May’s unemployment rate overshot its expectation, but the inherent volatility in the monthly data means that MPC probably won’t be willing to pause its hiking cycle just yet," he adds.

Thursday’s forecast update from the Bank of England will be every bit as important as the interest rate decision in determining the prospects of the Pound up ahead, particularly in the face of implied financial market expectations for three further increases to take Bank Rate from 5% to 5.75% by year-end.

“They’ve got a number of further increases priced in for us. My response to that would be: Well, we’ll see,” Governor Andrew Bailey said at a European Central Bank (ECB) conference in June and at a point when interest rate swap markets were suggesting a peak in Bank Rate of almost 6.5%.

Above: Quantitative model estimates of ranges for the week ahead. Source Pound Sterling Live.

Inflation has fallen since then and in the process kept alive hope and scope for something like the BoE's May forecasts still materialising in the months ahead: Back then the BoE had looked for inflation to reach 7% in July and something like 4% by year-end.

These forecasts still imply a positive real or inflation-adjusted ‘risk-free’ interest rate when the real economy is underperforming the trend growth rate of the pre-pandemic period when it was implied in the calibration of monetary policy that a modestly negative real rate was necessary to hold the economy up.

This could mean there is a high risk of markets being disappointed Thursday or further down the line in what would be a downside risk for Sterling and the Pound to Euro rate.

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of selected downtrends indicating possible areas of technical resistance for Sterling.

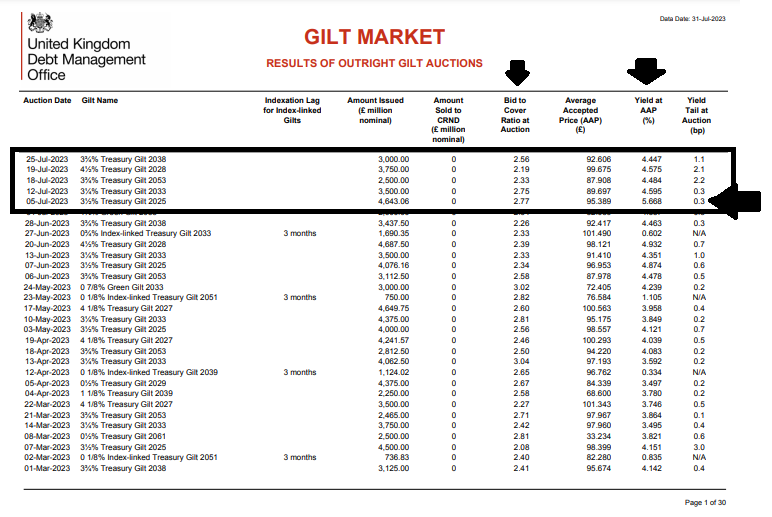

One of the more important events ahead of Thursday, however, is the 02-year government bond auction on Tuesday where the yield and any change in the number of bidders for every bond sold could offer valuable information after borrowing costs there reached the highest since 2007 earlier in July.

{kind=link}

“Fitch reports that the UK is now set to have the highest debt interest costs in the DM thanks to higher proportion of inflation-linked gilts relative to other markets (at roughly 25%),” says Bipan Rai, head of North American FX strategy at CIBC Capital Markets.

The early July bid-to-cover ratio illustrated robust demand for government debt when also nearing post-crisis highs earlier this month but any difference on Tuesday would be implicit insight into the market view on how the inflation and interest rate outlooks have or haven’t changed among real money buyers and sellers.