Pound Sterling Backed by Decisive 50bp Bank of England Hike

Above: Bank of England, City of London. Picture: Geoff Henson. Licensing: CC 2.0. Source: Flickr.

The Bank of England grasped the seriousness of the UK's inflationary pressures by opting to raise interest rates by 50 basis points, a move that Pound Sterling Live reported was a bare minimum if the Pound's 2023 gains were to be defended.

Indeed, the Pound showed some characteristic volatility in the wake of the decision but ultimately ended the day higher against the Euro and a host of other major currencies, although a broadly stronger U.S. Dollar continued to reclaim lost ground.

The Monetary Policy Committee (MPC) voted by a majority of 7–2 to increase Bank Rate by 50bp to 5.0%, in what amounts to a strong 'hawkish' signal.

But in a farcical development, two members of the MPC - Tenreyro and Dhingra - opted to keep interest rates unchanged.

"The second-round effects in domestic price and wage developments generated by external cost shocks were likely to take longer to unwind than they had done to emerge. There had been significant upside news in recent data that indicated more persistence in the inflation process, against the background of a tight labour market and continued resilience in demand," said the Bank in a statement.

It stated it would be prepared to raise interest rates further if the data warranted, confirming its data-first approach remains in place.

"The MPC did the right thing, raising the Bank Rate by 0.5pc to 5pc. A strong signal was needed to combat the stickiness of inflation and the threat of rising wage inflation. For once, the Committee has acted boldly and this should help return inflation to a downward path," says Andrew Sentance, a former member of the MPC and a critic of the Bank's go-slow approach to dealing with inflation.

Looking at the foreign exchange market reaction we can see a knee-jerk move higher by the British Pound which confirms the initial 'hawkishness' signalled by the 50bp move and the 7-2 majority. This gave way to some volatility but the Pound to Euro exchange rate closed the day 1.1627, which was slightly higher than where it opened. The Pound to Dollar exchange rate spiked to 1.2830 before retracing to close the day at 1.2747.

Ahead of the decision, markets were priced for Bank Rate to rise to as high as 6.0% by the time the MPC was done with this cycle, an expectation reflected in rising UK bond yields and the Pound.

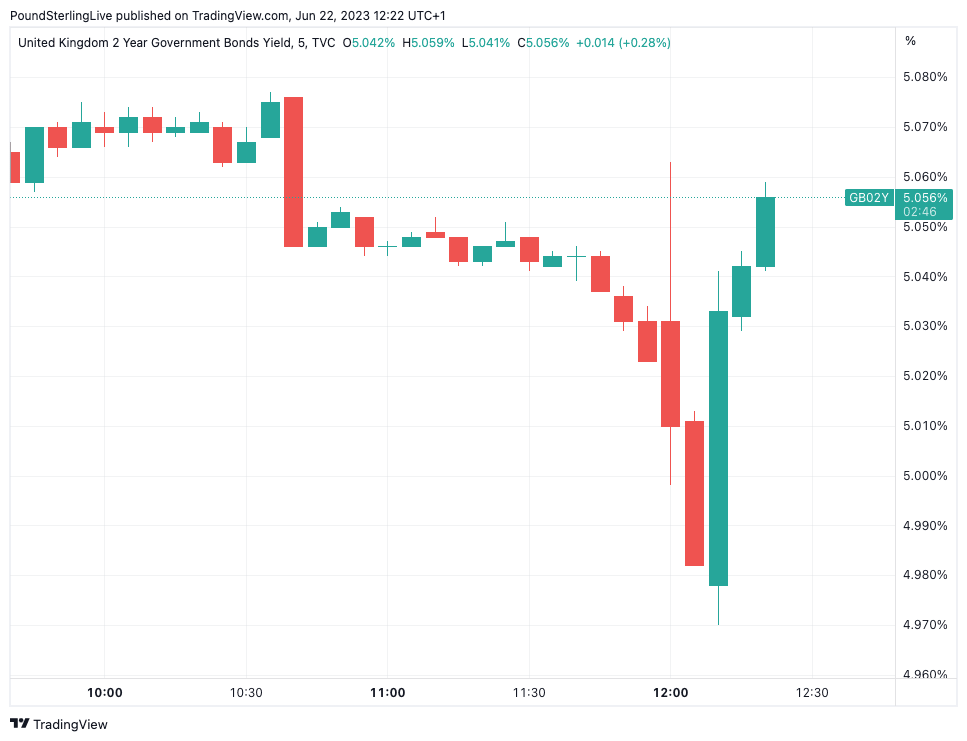

Interestingly, the UK two-year bond yield - the key yardstick for UK finance products such as mortgages - actually fell following the 50bp hike.

This could suggest some relief that the Bank is showing a more decisive approach to the country's inflation problem and signals the market believes that by going 'hard' now the Bank can get a grip on inflation, meaning it does not have to take Bank Rate as high as 6.0%.

"They have done us a favour and gone with 'just get on with it'," says Jordan Rochester, FX strategist at Nomura.

"I suspected knee-jerk GBP strength on the 50bps at first, but ultimately this could lower the odds of more hikes needed later this year," he adds.

Above: UK two-year bond yield reaction to the BoE hike.

Joseph Little, Global Chief Strategist at HSBC Asset Management says a "hawkish super-hike" comes in the context of this week’s disappointing inflation print and a widespread recognition that UK policymakers now need to "get ahead of the curve".

But a key downside risk to the Pound further out is that the steep rise in interest rates prompts a sharp slowdown in economic activity over the coming months, which then prompts the Bank to cut rates sharply.

"After the fastest rate tightening cycle since the 1980s, getting more hawkish now is not without risk. A looming ‘mortgage squeeze’ and a turn in the credit cycle means that the economy now faces a recession as we head toward 2024," says Little.

Short-term, the evidence suggests the Pound will however remain broadly supported by elevated Bank of England rate expectations, which could keep it in touch with recent multi-month highs against the Euro and Dollar.

Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics, points out the MPC demonstrated its determination to get a grip on domestically-generated inflation by choosing to omit any language designed to assure investors that the peak might be near.

"With the Committee showing little hesitation today to opt for a 50bp hike, and services CPI inflation likely to take a while to roll over, we now expect Bank Rate to peak at 5.50%, with 25bp hikes in August and September," he adds.

This would give the joint highest base rate of the developed economies, offering Pound Sterling support.

"Sterling overnight rates at 5.00% will now be high by reserve currency standards – making sterling an expensive sell," says Chris Turner, Global Head of Markets and Regional Head of Research for UK & CEE at ING Bank.

He explains the sharply inverted UK yield curve - whereby short-term bonds are higher than longer-term bonds - makes it even more expensive for foreign investors in the UK Gilt market to hedge currency exposure.

"Foreign bond investors lowering FX hedge ratios could prove a net sterling positive," says Turner.

Following the Bank of England's decision, ING's strategists are happy with a year-end GBP/USD forecast for 1.33 a return in EUR/GBP to the 0.88 area (GBP/EUR to 1.14).