Reasons Why Pound Sterling Might Struggle to Rise Much Further

"He was not to blame for the statistical underestimation of economic strength in 1987-88. But a more cautious approach to fiscal and monetary policy would have been justified" - OMFIF.

Image © Adobe Stock

Pound Sterling outperformed many other major currencies in the opening months of the year and remained buoyant through much of this week but there are two reasons why Bank of England (BoE) interest rate policy might now be an asymmetric risk on the downside for the months ahead.

Sterling eased from near earlier highs against most major currencies on Thursday but was still close to being an outperformer for the week while carrying gains over most of its G20 counterparts for 2023 after extending in the opening quarter the recovery that began at record lows late last year.

Many attribute gains to barometers suggesting an economy that has outperformed the often-imperfect forecasts of the Bank of England (BoE) even as it has slowed to a crawl speed, though with inflation remaining in the double-digits last month, Sterling's time in the sun might be almost up.

Inflation fell to only 10.1% last month in contrast with economist expectations for a fall back into the high single digits, leading interest rate markets to price a high probability of Bank Rate being lifted from 4.25% to almost 5% as a result and potentially posing risks to Sterling going forward.

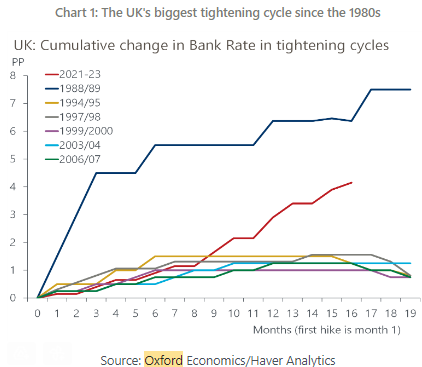

"Moreover, the consensus for UK policy rates three or four years ahead has risen from 1%-2% in 2019 and around 1.25% in late-2021 to about 3% recently," says Michael Saunders, a senior adviser at Oxford Economics and a former member of the BoE's Monetary Policy Committee.

Source: Oxford Economics.

"We suspect that this tightening cycle is now largely over, with probably a final 25bp hike in May. The economy has been flat-lining since mid-2022, while the lagged effects of the recent large policy tightening are likely to weigh on activity and produce a sustained rise in spare capacity in the coming quarters," he adds.

Oxford Economics is just one of many firms doubting whether Bank Rate will actually need to be lifted as far as financial markets currently envisage, and should these voices turn out to be right then an eventual correction of market expectations would likely weigh heavily on the Pound in the near future.

But whether or not these do turn out to be right likely hinges on the inflation figures coming from the UK over the coming months, particularly in the context of the BoE's February forecasts, which suggested a rapid second-quarter fall would put the inflation rate on course for around 4% at year-end.

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |

"While we expected some outperformance in GDP and wage growth, relative to the Bank's projections, we highlighted downside risks to CPI and credit conditions. Since the March meeting, all key metrics have outperformed our expectations," says Sanjay Raja, an economist at Deutsche Bank.

"We expect the MPC to stick to its current data-dependent message in May. And importantly, we now see risks to our terminal rate forecast skewed to the upside," Raja writes in a research briefing after lifting Deutsche Bank's endpoint forecast from 4.25% to 4.75%. just last week.

The biggest risk for Pound Sterling, however, is if inflation does not come down as far as is necessary in the coming quarter because this could necessitate even further increases in Bank Rate, and the economic damage that could ensue from those would hardly be helpful for the Pound

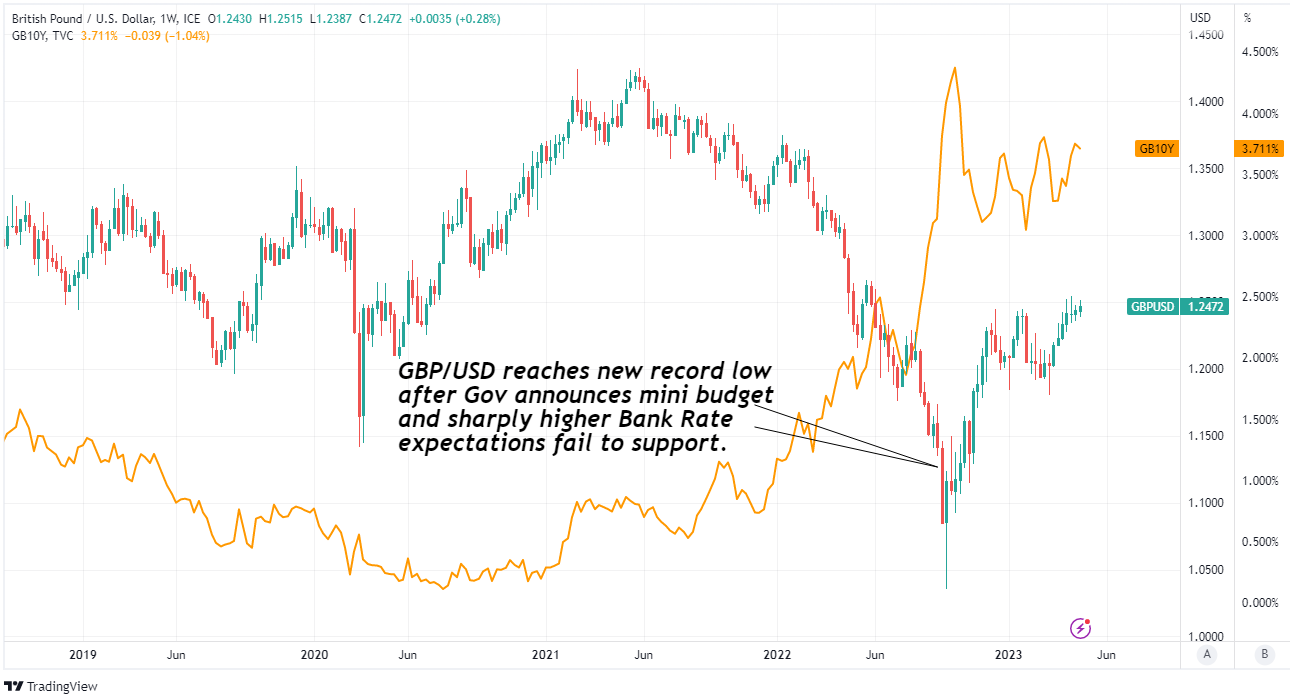

Above: Pound to Dollar rate shown at weekly intervals with 02-year UK government bond yield. Click image for closer inspection.

Above: Pound to Dollar rate shown at weekly intervals with 02-year UK government bond yield. Click image for closer inspection.

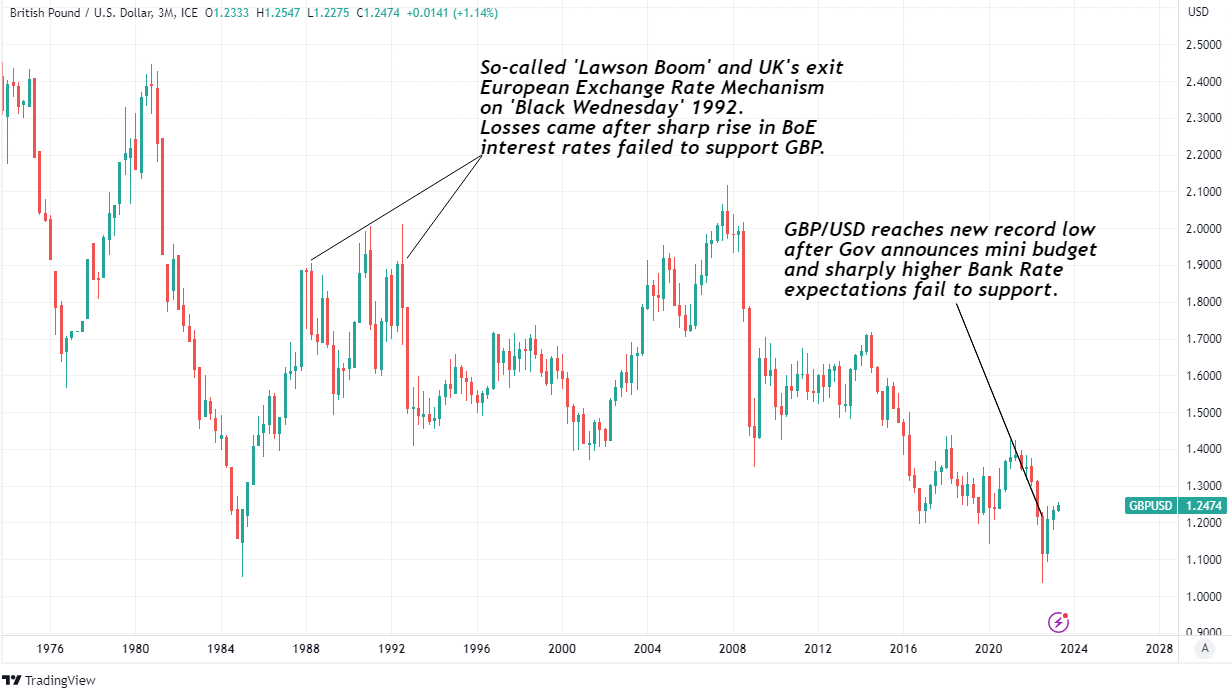

There are precedents demonstrating how economically damaging increases in Bank Rate can be taken badly by Sterling including the period when the budget of former Prime Minister Liz Truss led financial markets to bet last September that borrowing costs would then need to rise to 5.75% in 2023.

But the better example might be the infamous 'Black Wednesday' of September 1992 when the Pound fell out of the European Exchange Rate Mechanism despite a protracted period of very sharp earlier increases in interest rates from the late Chancellor Nigel Lawson.

"Lawson’s reaction was swift and decisive. He returned to a sparsely populated Whitehall and engineered an immediate 1 percentage point rise in interest rates. This was followed by two further 1-point rises," says Peter Sedgwick, a HM Treasury adviser to the late Chancellor Nigel Lawson.

"He was not to blame for the statistical underestimation of economic strength in 1987-88. But a more cautious approach to fiscal and monetary policy would have been justified," Sedgwick adds in a Tuesday article for the Official Monetary and Financial Institutions Forum (OMFIF).

Readers can get more of Sedgwick's story surrounding the events of Black Wednesday here.

Above: Pound to Dollar rate shown at 3-month intervals. Click image for closer inspection.

Above: Pound to Dollar rate shown at 3-month intervals. Click image for closer inspection.