Euro-Dollar: Take Cash off the Table Ahead of ECB Traders Warned

EUR/USD rally to fade as traders adopt caution ahead of upcoming ECB meeting.

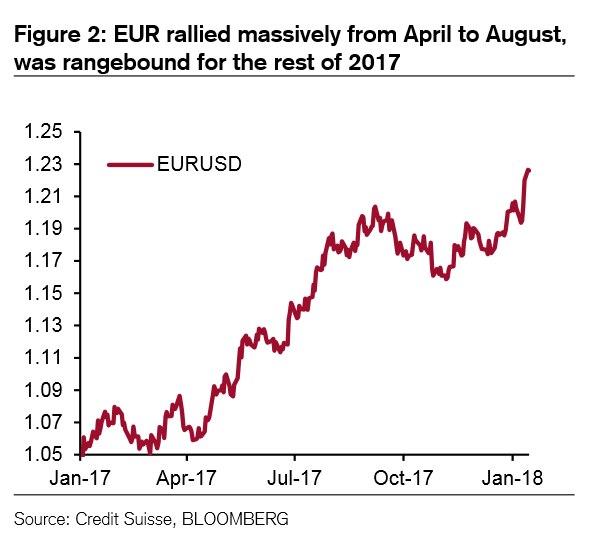

After rising a staggering 13% between March and August 2017, it might just be time to book profit on the EUR/USD exchange rate rally.

Strategists at Credit Suisse are one notable player who reckon the Euro's rally could be undermined - on the short-term at least - by the European Central Bank (ECB) meeting, on January 25.

"Our view has been to be long EURUSD structurally... but to look to take profits or at least scale back ahead of the ECB meeting on 25 January," says Credit Suisse analyst Shahab Jalinoos.

There is increased speculation that the governing council of the ECB will seek to talk the Euro lower, indeed recent communications from various members of the council confirms many are growing uncomfortable with the Euro's recent rise saying it undermines their effors to boost inflation to their mandated 2.0% target.

The call to sell, "holds especially if EURUSD is trading materially above the recent breakout level around 1.21 going into next week, and we would become still more convinced that this is the right thing to do if EURUSD is close to 1.25 before the ECB meeting," says Jalinoos.

Credit Suisse believe there exists a material risk that either the policy statement produced at the meeting or the comments from ECB President Mario Draghi afterward will drag on the Euro.

This dovetails with the increasingly held view that the Euro may be getting so strong it will become a severe headwind to getting inflation back up to 'normal' levels at a touch below 2.0%, by making imports cheaper.

Already this week, three members of the ECB governing council have commented that the level of the Euro should be watched carefully watched, observed or is outright too high and will hamper the return of normal inflation levels, the fostering of which is part of the remit of the ECB.

Jalinoos also sees heightened risks for the Euro as January draws to a close from the market starting to look ahead and price in another risky event, the Italian general election in March.

Yet the tactical call to sell in the short-term contrasts with Credit Suisse's longer-term outlook in which they are very bullish and expect the EUR/USD to climb to new highs.

As such they see any pull-back an opportunity to buy on dips, getting in at a better price - and to this end - they highly recommend buying on any moves into the 1.18-1.20 zone in particular.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.

Structurally Bullish

Credit Suisse have seven reasons why they are bullish the Euro versus the US Dollar in the long-term:

1) Despite the differential in interest rates ostensibly favouring the Dollar where they are higher and expected to rise, the reality is the Euro has kept rallying rather than fallen to narrow the divergence, following every positive news-bite. Credit Suisse's is stance is that the wide differential is a reason holding back the Euro from rallying more rapidly, not a reason to expect the US Dollar to appreciate.

2) The Eurozone has a large current account surplus which is positive for the currency as it is, however, as the Euro-area economy improves - as it is widely expected to - the outflows which would normally recycle the surplus in the form of foreign asset investments is likely to fall rather than increase, raising, what is called the Euro's 'clearing rate'.

3) The cost of tax reforms is expected to exacerbate the US budget deficit. The US already has a wide trade deficit, having both at the same time (twin deficits), especially when they are steepening is generally bad for the Dollar.

4) Political risk is now arguably greater in the US with more trade protectionist stirrings than in Europe given the recent strides made in Germany to form a coalition and the very low probability of an anti-Euro party gaining leverage in Italy.

5) Market positioning is not as imbalanced as some analysts have argued, according to jalinoos, who thinks traders were not as heavily long the Euro and short the Dollar over Christmas because of the risk tax reform might give the Dollar a boost. If true there is less reason to expect a backlash against the Euro.

6) Longer-term valuation methods state 1.30 as a fair-value exchange rate for EUR/USD so arguments that it is already overvalued are over the top, argues Jalinoos. Even though it rose 13% in 6 months in 2017, it then pulled back and went sideways at the end of the year and so probably isn't dangerously overbought.

7) When global growth rises history suggests the EUR/USD does as well. This is because Eurozone exports benefit, general optimism covers the cracks in the Eurozone's imperfect fiscal and political conditions, and emerging market central banks restock their Euro reserves.

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.