UBS Warn GBP/EUR Rate Could go as Low as €0.95

The Pound to Euro exchange rate is destined to either maintain familiar levels to the present, go above 1.20 or dip below 1.0 according to new insights provided by UBS.

New predictions for Pound Sterling against the Euro have been released by UBS who have presented clients with three scenarios; the most notable of which sees the GBP/EUR falling below 1.0 within a year.

But, another sees the exchange rate rising back above 1.20.

According to analysts at the Swiss lender, the scenario that ultimately comes to pass will depend on the support delivered to the currency by UK corporates with foreign operations.

According to a new research note released May 31, UBS say income earned by UK companies abroad may be a providing underlying support to the Pound and many in the analyst and commentary community have been missing this key factor.

As such, the outlook for Sterling will ultimately come down to how this factor plays out.

UBS say the repatriation of strong earnings from abroad is a major reason behind Sterling’s relative resilience and the better-than-expected performance of the Euro to Pound exchange rate (EUR/GBP) so far in 2017.

The rising inflows of income earned abroad are keeping demand for the Pound relatively strong.

“The market debate around Sterling may be missing a key point; post-referendum economic resilience, BoE policy, Brexit pricing-in and positioning all play a role but are arguably not the decisive factors in determining Sterling's path,” says analyst Lefteris Farmakis at UBS.

“Instead, substantial improvements in the current account may have significantly boosted Sterling,” added the analyst.

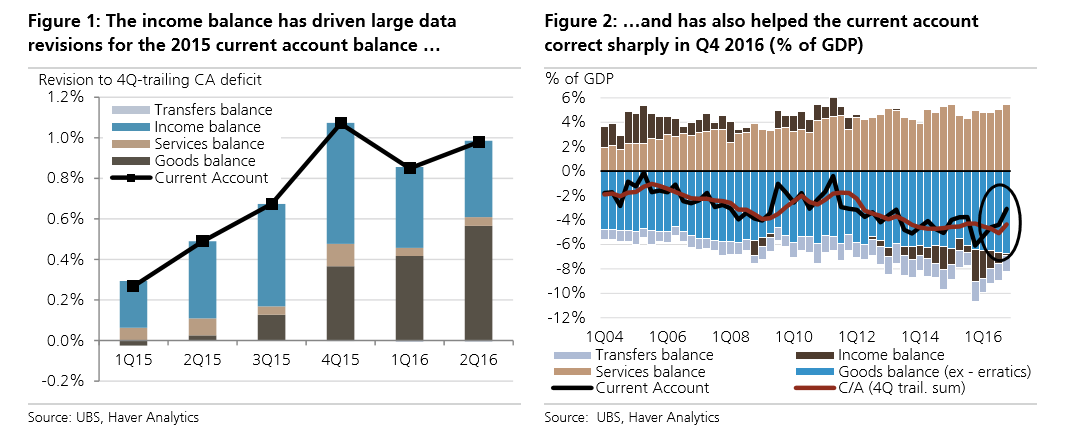

The main component to have risen within the UK’s current account is the ‘income balance’ which is the net flow of income earned by Britons abroad which is repatriated.

Income earned abroad has risen due to global reflation and a widespread rise in global growth, which has supposedly added 1.5% to the income balance over the last year.

This, more than the increase in UK exported goods due to the weak Pound, has helped reduce the current account deficit, which measures net inflows in their totality.

Therefore the strength of the global economy - and especially the Eurozone - are a major reason why Sterling has not collapsed further in the wake of the EU referendum.

Looking ahead then, the future of Sterling may be more dependent on wider global growth than previously thought.

Brexit-Related Risks "Skewing the Balance"

But this is not the only factor impacting on the Pound, more quotidian concerns are still a major influence.

Brexit fears, for example, are seen as a major contributor to the currency’s valuation matrix.

“Brexit-related risks are skewing the balance further to the downside. A harder Brexit than currently anticipated by markets has the potential to lead to a sharper moderation in the capital flows needed to cover the current account gap,” said Farmakis.

Of most concern in relation to Brexit is the UK’s large services surplus with the EU which could come under threat in a hard Brexit scenario.

“In addition, the services balance, which is heavily in surplus and supports the current account, may prove a special source of vulnerability due to its reliance on the financial services sector,” says the UBS analyst.

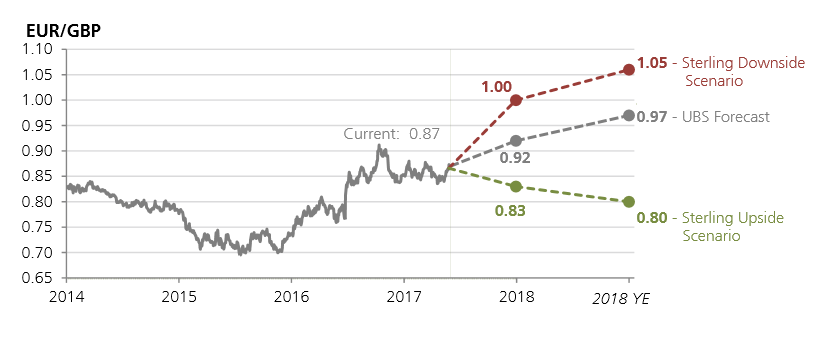

Three Forecasts for the Pound v Euro Rate

Farmakis dismisses arguments that the June election is likely to lead to a softer Brexit outcome and actually sees signs of vulnerability for Sterling on the horizon – especially if polls prove accurate.

The analyst moderates his GBP forecasts, although risks remain skewed to the downside.

He sees EUR/GBP rising to 0.92 by end-2017 and 0.97 at end-2018 (from 1.00 for both years previously), effectively foreseeing a more gradual weakening of the currency due to the benign influence of income balance.

From a Pound into Euro exchange rate perspective this translates to 1.0869 and 1.0309.

However, despite the undertow from the income balance there is a risk the global upcycle will place this source of strength in jeopardy.

“Brexit risks remain acute, all the more so if they materialise during a cyclical downturn,” says Farmakis.

The UBS analyst paints three broad future scenarios for EUR/GBP.

The first scenario sees GBP weakening substantially to 1.00 versus EUR in 2017 and 1.05 in 2018, due to a combination of hard Brexit hitting the services balance and the global growth cycle rolling over and thus thinning down the income balance.

1.05 in EUR/GBP equates to 0.95 in GBP to EUR terms. This will be a startling finding for many watching this market.

The second scenario is UBS’s base case, has already been mentioned, sees Sterling depreciates but at a more modest pace to scenario 1.

The second scenario is based on a hard Brexit combined with a continued upcycle in global growth supporting inflows via the income balance.

The third scenario sees a softer Brexit in which the UK retains free trade with the EU, especially the UK services and financial services sectors, combined with a continuation of the upcycle in global growth producing robust inflows via the income balance.

This sees 0.83 and 0.80 being the targets for the two timeframes.

This equates to GBP/EUR at 1.2048 and 1.25.

Those concerned about any potential moves lower should consider setting up a strategy to protect against such a move. Get in touch with a specialist here.

Pound to Euro Rate Closes Week Sharply Lower

The British Pound fell sharply against the Euro ahead of the weekend amidst a broad-based rally in the European currency.

There was no immediate sign of any Sterling-related reason for the sell-off.

Rather, the culprit appears to be the Euro which according to one analyst “got its groove back” after slower U.S. hiring inspired a fresh round of Dollar selling.

“The Euro earlier in the week had its gains checked after Eurozone inflation slowed more than expected, suggesting less scope for the ECB next week to sound a hawkish note,” says Joe Manimbo, an analyst with Western Union.

Key for the Euro going forward will be the extent to which officials signal a chance of reducing stimulus in the months ahead.

“Failure to open the door to reduced stimulus this year would leave the Euro ripe for a corrective move lower,” warns Manimbo.

The ECB next meets on June 8 and no change to its low rate policies is expected, but officials could sound a more cheerful note with inflation out of a deflationary zone and unemployment trending lower.