UK GDP Jump Likely to Prove Short-lived: Economists

- Written by: Gary Howes

-

Image © Adobe Images

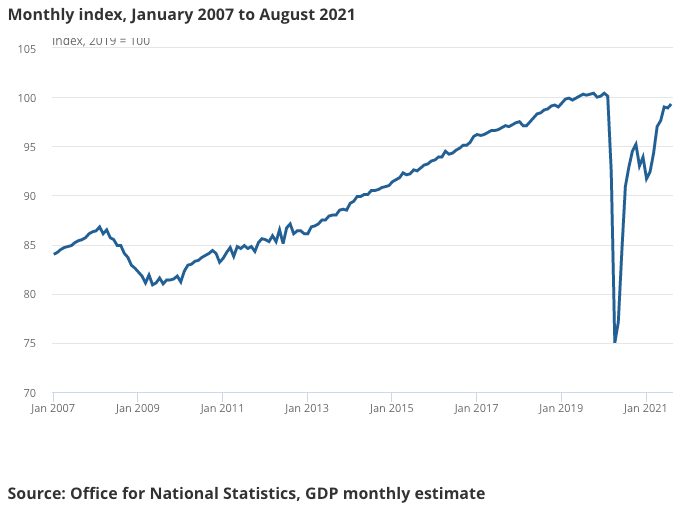

UK GDP grew 0.4% month-on-month in August 2021 as the economy began to expand again following a 0.1% decline in July, however some economists warn growth has almost certainly flatlined since then.

The 0.4% growth figure does however underwhelm slightly against the market consensus expectation for GDP growth to come in at 0.5%.

The economy grew 6.9% year-on-year in August says the ONS, beating expectations for a figure of 6.7% but coming in below the 7.5% expansion posted in July and UK GDP now remains 0.8% below its pre-coronavirus pandemic level.

"The improvement in August probably had a lot to do with the fading of the restraint from July’s 'pingdemic', which at one point meant more than 1m people were self-isolating," says Paul Dales, Chief UK Economist at Capital Economics.

Simon French, Chief Economist at Panmure Gordon says the underlying growth rate was in fact better than the headline suggests owing to headwinds provided by the Test & Trace programme.

Testing for Covid has subtracted a sizeable 0.3% from the monthly growth figure, suggesting to French that underlying UK growth was at 0.7% month-on-month.

Helping the economic recovery was growth in the services sector, which accounts for over 80% of UK economic activity. The ONS says services output grew by 0.3% in August, a recovery from the fall of 0.1% recorded in July.

Accommodation and food service activities, arts, entertainment and recreation contributed most positively to services growth in August 2021, partially offset by falls in health output and retail trade.

Underscoring economic growth was a recovery in industrial production which saw a 0.8% increase in activity month-on-month in August, coming in well ahead of the 0.2% expected by the consensus.

But this is down slightly on the 1.2% growth recorded in July.

Industrial growth expanded mainly because of the continued increase in the extraction of crude petroleum and natural gas following the recent temporary closure of oil field production sites for planned maintenance.

Manufacturing production meanwhile rebounded 0.5% month-on-month in August, up from 0.2% in July and beating consensus expectations for growth of just 0.1%.

A 6.6% month-on-month rise in car production was the second increase in a row "and suggests that the semiconductor shortages may be easing," says Dales.

Continuing UK economic expansion comes amidst falling unemployment and rising wages, leading to speculation the Bank of England could lift interest rates as soon as November.

While the prospect of a rate hike has grown in the light of the economic recovery the more pressing reason for a hike is the surge in inflation, and concerns at the Bank of England that it could become enduring.

The GDP data released on Wednesday is robust enough to keep expectations for a rate rise alive, however there are concerns growth has since stalled again.

"The recent broadening in shortages and the fuel crisis may mean that growth has come to a near-standstill since August," says Dales.

"The UK economy may have weathered the Delta Covid-19 wave better than we'd feared, but the recovery is nevertheless slowing," says James Smith, Developed Markets Economist at ING Bank.

Market's are now fully priced for a 10 basis point rise in November, but these expectations face disappointment if concerns over surging energy prices, labour shortages and ongoing supply chain disruptions prompt members of the Bank of England's Monetary Policy Committee to refrain from raising interest rates.

"A weaker activity outlook means it’s not a done deal," says Dales.

Capital Economics predict GDP may have risen by around 1.4% quarter-on-quarter in the third quarter, which would be weaker than the 2.1% rise the Bank of England expected as per their September polciy update.

"Recent BoE commentary suggests growth is unlikely to be the biggest factor in the committee's decision to hike interest rates over coming months – though it does offer a reason for caution. We still suspect policymakers will wait until 2022, when more information on wage growth will be available, before hiking," says ING Bank's Smith.

ING expect fourth-quarter growth will get a boost from the return to schools and the noticeable increase in office activity.

"But it’s still likely to take until early next year before economic activity hits pre-virus levels, and our 1% growth forecast for the fourth quarter is again lower than the BoE’s," says Smith.