Swiss Franc Strength Confounds Clients of Goldman Sachs

- Written by: Gary Howes

-

Image © Adobe Images

- GBP/CHF reference rates at publication:

- Spot: 1.2526

- Bank transfers (indicative guide): 1.2088-1.2175

- Money transfer specialist rates (indicative): 1.2413-1.2438

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The Swiss Franc's multi-week run of gains might have as much to do with a positioning unwind as it does with a recent spike in investor demand for 'safe haven' assets, according to new research from Goldman Sachs.

In a weekly currency briefing the investment bank addressed Swiss Franc dynamics following a rise in client queries concerning the currency's recent volatility.

The value of the Franc has increased since about April and comes even as global stock markets were appreciating in a 'risk on' trend.

Typically, a safe haven such as the Franc would be expected to depreciate in such an environment.

Yet the Franc has maintained its safe haven credentials, rising last week when stock markets were falling amidst investor fears that a global growth slowdown caused by the spread of the Covid delta variant was hurting global economic growth prospects.

"While it certainly aligns with broader market moves to price lower growth and higher 'left tail' risks, we think that is only part of the story," says Zach Pandl, co-head of foreign exchange strategy for Goldman Sachs.

Goldman Sachs find the Franc might be the beneficiary of a major unwind in crowded positioning, a phenomenon whereby a currency that was once heavily sold as part of a popular trade finds support as those positions are closed.

Selling the Franc was a popular bet in early 2021 as part of the global 'reflation trade', which coincided with a rapid deprecation in the currency's value during the first three months of 2021.

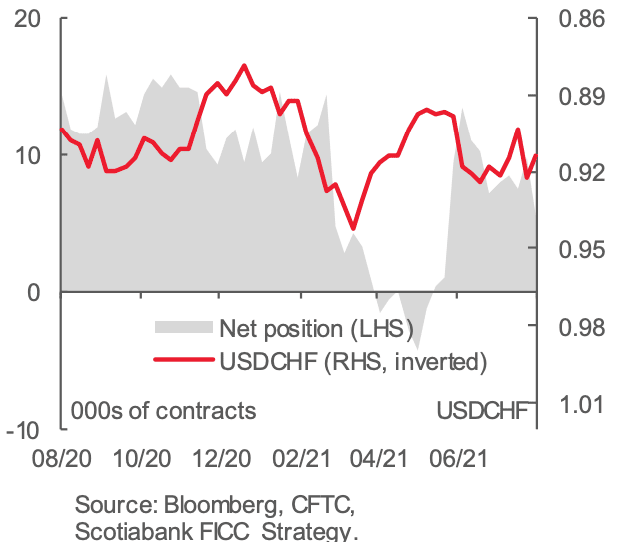

Market positioning data from the CFTC - the most comprehensive dataset of its kind - shows that there was a surge in popularity in the "sell CHF" trade in the early part of the year, but this has since unwound:

Image courtesy of Scotiabank.

The Franc has been notably robust since early April and has appreciated against both the Euro and Pound, suggesting that the "sell CHF" trade might have become overcrowded and was in the process of unwinding.

"With market attention turning from reflation to a more staggered recovery, crowded trades have been under pressure, and we think the data suggests that recent Franc strength is likely driven by this dynamic," says Pandl.

The market experienced a particularly strong impulse of demand for the Swiss unit last week when the Pound-to-Franc exchange rate fell 1.63%, leaving it quoting at 1.2525 at the time of writing.

The Euro-to-Franc exchange rate fell 0.64% last week and is quoted at 1.0733, the the Dollar-to-Franc exchange rate meanwhile eked out a 0.18% gain and is seen at 0.9145 at the time of writing.

Above: Weekly chart of GBP/CHF (top) and EUR/CHF (bottom).

Secure a retail exchange rate that is between 3-5% stronger than offered by leading banks, learn more.

Goldman Sachs modelling finds EUR/CHF has fallen by more than it would typically be expected to fall when markets are falling and they say the Franc’s behaviour has been comparable to other European safe haven assets like 5y German bunds.

"But EUR/CHF risk reversals show little signs of stress, and are currently positive out to three months, which indicates that recent strength is likely driven by position liquidation, rather than safe haven demand like in Q2 2020," says Pandl.

On the perennial question of whether strength in the Swiss currency is about to elicit intervention from its central bank, Goldman Sachs note sight deposits at the Swiss National Bank (SNB) have picked up slightly in recent weeks, but analysts do not yet see clear evidence that the central bank has stepped in to curb strength in the currency.

But Jeremy Boulton, a market analyst at Reuters says EUR/USD is usually underpinned during bouts of SNB intervention.

"Surprise EUR/CHF and EUR/USD upticks may be signs SNB has returned to market," says Boulton.

The Franc's rapid decline in the first three months of 2021 will have taken pressure of the SNB to intervene, but investors are questioning whether the ongoing robust trading in the exchange rate will prove a source of frustration to policy makers.

"As the global growth cycle is about to slow, CHF appreciation is about to test the SNB reaction function. EURCHF tested 1.07 several times last week, the lowest level seen since the synchronised rally in risk assets got going for real last November," says Magne Østnor, an analyst with DNB Markets.

DNB Markets anticipate the global growth cycle to slow further allowing the Franc to be supported "for some time".

Goldman Sachs however maintain a view that the settings remain in place for a resumption in the depreciation of the CHF.

"We still think the fundamental outlook points to a weaker Franc ahead, but it will take some stabilization in the global growth outlook for this trend to resume," says Pandl.