Australian Dollar at Risk of Weakness as Commodity Price Decline to Extend

The Australian Dollar is likely to weaken over the medium term on the twin effects of a fall in Chinese demand for Australian commodities and slowing domestic wage growth.

Starting with China, speculation that Chinese demand for the two key Australian commodity exports – Iron Ore and Coal - is forecast to wane.

The introduction of greater regulation in both commodity futures speculation - which had eclipsed real deliverables futures trading in importance - and borrowing in the all-important property sector put a squeeze on Iron Ore and Coal demand.

Incentives for companies using a higher-grade Iron Ore from Brazil which causes less pollution, was yet another negative development for the Aussie, which saw their contribution to the total Iron ore supply in China fall by 5% (from 55% to 50%) as a result.

According to Morgan Stanley’s Has Redeker, there appears to be a general reluctance to “add debt to the low productivity ‘old’ economy,” in China with the emphasis now more on rebalancing the economy in favour of services and domestic consumption.

“Falling China-related commodity prices should put the AUD under selling pressure,” says Redeker, in a note seen by Pound Sterling Live.

But it is not just a retraction in the demand side of the equation – there is a supply glut problem too.

“Factors such as Vale's S11D roll-out and dormant supply in Australia should cap prices, in our commodity analysts' view. Put together with the demand side, with the current rate of Chinese steel production and on-going steel capacity reform, our commodities team forecasts iron ore at $74/tonne by year-end, implying 11% further downside in 2017 and more to come in 2018,” says Redeker.

Vale’s S11D mine in the Amazon Basin is expected to be the largest in the world and may well further increase Brazil’s contribution to Chinese Iron Ore imports even further, given the superlative quality of Amazonian Ore.

Restocking Season at an End, Iron Ore to Recover say Macquarie

According to a recent report from Macquarie, Iron Ore will probably witness a decline soon due to the restocking season reaching an end, as normally happens in Q1.

Macquarie see this as just a seasonal factor and Iron Ore will recover.

They also see steel prices remaining high as we enter an intense period of steel production following the stocking up of store houses, with its constituent elements.

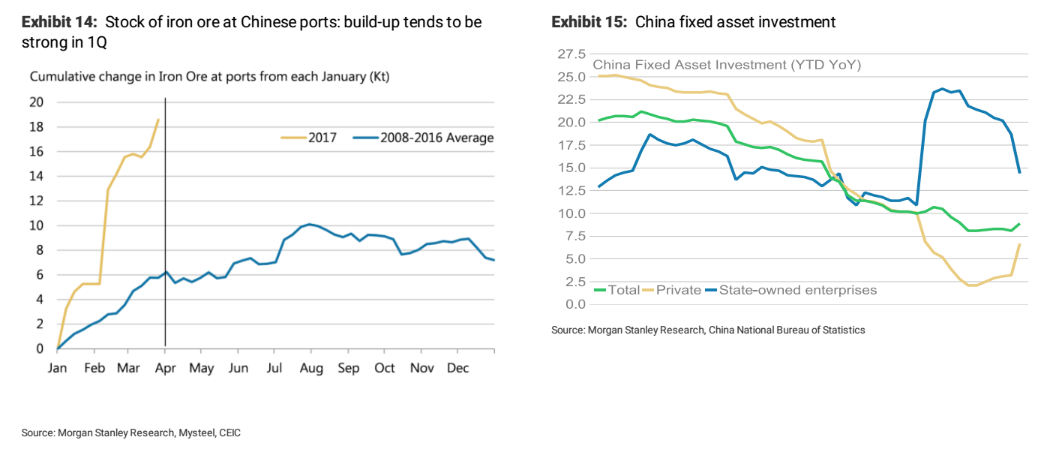

The restocking season explanation, also explains Morgan Stanley’s view that Iron Ore imported to Chinese ports has been running very high vis-à-vis consumption implying an inventory overshoot, highlighted by the build-up of Iron Ore in Chinese ports.

Slow Australian Wage Growth Could Weigh on AUD

Another expected pressure on the Australian Dollar comes from low wage growth.

The relationship may not be immediately apparent but is due to the high impact on inflation of wages.

Inflation in Australia is running below average and this is keeping interest rates down, which are set by the Reserve Bank of Australia (RBA).

Low interest rates weigh on a currency as they attract less flows from international investors who prefer higher interest rates because it gives them a better return on their money.

Thus, slow wage growth is keeping inflation low which in turn is keeping cap on the Aussie Dollar.

“There are many explanations for low wages growth, including rising spare capacity in the labour market, heightened job security concerns, low inflation rates and declining commodity prices from the peak in 2011,” comments Commonwealth Bank’s senior FX strategist Stephen Capurso.

The labour market in Australia is not particularly strong as illustrated by the high number of people who work part-time, want to work longer, but can’t.

“Underemployment measures people that have a job but would like to work more hours. The underemployment rate is now at a record high of 8.7%. Job security concerns also remain elevated. The combination of underemployment and job security concerns means that people are unwilling to push their employers for a pay increase,” added Capurso.

The strategist also notes the negative feedback loop between low inflation expectations and low wage expectations.

Low inflation and inflation expectations make workers less likely to demand higher pay deals compared to when inflation is high.

Many wages rises are also set according to inflation expectations.

“Inflation expectations have in impact on inflation outcomes, and many wages are set with the CPI outcome in mind. Awards and minimum wage outcomes set by the Fair Work Commission are heavily influenced by the CPI,” said Capurso.

Stuttering commodity prices will not help elevate wages, especially not in the mining sector, and if iron ore and coal fall as much as expected on reduced China demand this may also feedback into lower wage growth more generally too as the impact fans out into the rest of the economy.

Wages growth in Q1 2017 is forecast to remain muted and to lead to a minor growth tick in inflation, but probably not enough to push up the AUD.

“We already have the underemployment rate for Q1 so we can use our model to forecast wages growth for the March quarter. The model is pointing to a 0.5% rise in private sector wages. This would see the annual rate of growth tick up to 1.9%.”

With wages and inflation remaining so stubbornly low why doesn’t the RBA increase stimulus?

Commonwealth Bank say because of financial stability concerns, stemming from the rising level of household debt and strongly rising house prices in Sydney and Melbourne.

The suggest the RBA would prefer to see a slow return of inflation to its target rather than cut rates and see inflation rates increase but household debt rise even further.

They say the RBA is getting ever more entrenched in their position and the “rhetoric is getting stronger,” say Commonwealth, “with an acknowledgement in the latest Meeting Minutes that “there had been a build-up of risks associated with the housing market.”

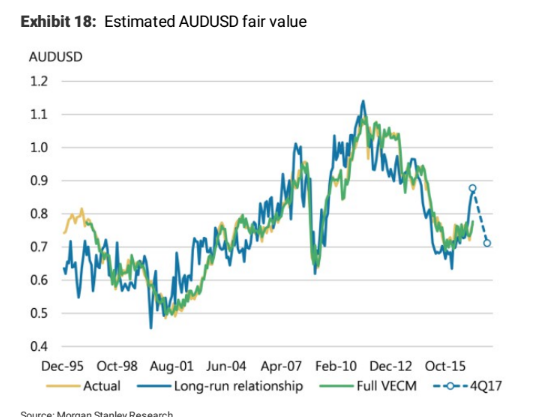

Forecast of 0.69

Morgan Stanley use a complex model to determine what the AUD/USD’s fair value should be and what it is likely to be at the end of the year.

The model includes inputs from the three main fundamental factors which determine the fluctuating value of the Aussie Dollar, interest rates and expectations, bond yields and their expectations and commodities prices and their forecasts.

This gives a current ‘fair value’ of about 0.87 (above the current 0.76 exchange rate) but a Q4 value of 0.71, as it is set to decline steeply.

“This analysis and the outlook for policy rates and commodities underscores our bearish view on the AUD, and we remain sellers of AUDUSD targeting 0.69 in the short-run. The risk to our trade is that iron ore prices start rising again due to stockpiling,” says Morgan Stanley’s Redeker.

Clearly the double whammy of falling commodities and persistently low pay is set to be a serious dampener across most Aussie pairs.