CBA's Australian Dollar Forecasts 2017: USD to Rule but AUD to Advance on EUR, GBP

- British Pound to Australian Dollar rate forecast to fall notably

- The Euro to Australian Dollar forecasts revised lower

- US Dollar to be dominant in 2017

The Australian Dollar is forecast to slide against the US Dollar in 2017 but should maintain strength against the British Pound and Euro.

This is according to the year-ahead foreign exchange forecasts laid out by analysts at Commonwealth Bank of Australia (CBA).

“We now adjust our currency forecasts to account for another 10% lift in the USD from today’s levels (a total 15% lift in the USD since the U.S. election), largely driven by Trump’s proposals to cut the U.S. company tax rate,” says Chief Currency Strategist at CBA, Richard Grace in a note seen by Pound Sterling Live.

US Dollar to Dominate

Like most institutional analysts, CBA is forecasting the cyclical period of Dollar appreciation to extend in 2017.

And it is around the US Dollar that forecasts for the other major currencies are slotted into place.

A cut in the corporate tax rate from 35% to 15% will raise after-tax profits and lead to a surge in US stock markets.

This, in turn, will attract massive inflows of foreign capital seeking to buy shares in US companies and ride the Trump bull higher.

A by-product of this will be increased demand for US Dollars.

It is unlikely such an unabashedly right-leaning policy will be vetoed by the Republican-controlled Congress.

If Trump does not reduce the company tax rate to 15% then the USD will not strengthen much more from current levels, and our forecasts will need changing,” concludes Grace.

Offshore Plunder

The other major driver for the Dollar will come from a repatriation of an estimated 2 trillion in corporate profits stashed overseas.

Trump is offering a one-off 10% tax rate for repatriations over a limited amnesty period.

The lower domestic tax rate is also expected to make companies less reluctant to repatriate earnings made in overseas subsidiaries in the future, hopefully avoiding another build-up.

Historical president seems to suggest repatriations are a major driver for USD.

“The surge in U.S. capital inflows over 2005 that dramatically lifted the USD following the introduction of the 2004 Homeland Investment Act company tax-holiday window, demonstrates how sensitive the USD is to multinational profit repatriation,” says Grace.

Goldman Sachs predicts that S&P 500 companies will bring back $200 billion of the $1 trillion in cash they hold outside the United States and use $150 billion for share buybacks.

With annual buybacks among S&P 500 firms running at a $592 billion annual clip through the second quarter, that's a big bump and one the market will greet with enthusiasm.

Amidst the USD’s counterparts, the Yen is expected to depreciate the most versus the rising buck.

“We believe the main outlet for USD strength will be against the JPY, and to a lesser extent, GBP, EUR, CAD, AUD, NZD and CNY.

“Overall, the USD will strengthen on a broad-based trade-weighted basis,” says Grace.

AUD/USD Forecast to Fall

The Aussie Dollar will be unable to resist the Greenback's push higher in 2017 say Commonwealth.

But, the Australian Dollar is not expected to weaken as much as other currencies during the Dollar’s rampage higher.

CBA give two main reasons why the Aussie will remain supported.

The first is a forecast rise in commodity prices.

Australia is a major commodity exporting country and any rise in the price of commodities leads to an increase aggregate demand for Aussie Dollars by the countries importing their exports.

The second main reason is suggestions from the Reserve Bank of Australia (RBA) that it will not cut interest rates any lower.

Interest rates are a major driver of the value of currencies.

When they are relatively higher they attract a higher influx of investor capital seeking higher relative returns on their investments.

“We believe the RBA has finished cutting interest rates. The RBA has made the observation that “globally, the outlook for inflation is more balanced than it has been for some time,” says Grace.

Indeed, the higher prices expected to be commanded by Aussie commodities will contribute to increased inflation and is more likely to lead the RBA to push up interest rates rather than cutting them.

Chinese Gamble

CBA’s forecast does rely on continued demand from China, but this is not a given argue analysts at Bank of America Merrill Lynch.

Analysts at the US investment bank see dark clouds on the horizon for the Chinese economy, which, is probably about to face a credit crunch.

The huge amounts of debt taken on in China during the boom years, particularly in the property sector, make China vulnerable to a credit crisis.

Either a rise in inflation or a slowdown in the economy could see defaults rise leading to a financial crisis.

This would substantially impact on Chinese demand for Aussie commodities.

“While the ongoing unwind in USD longs will support the AUD in the short-term, we believe USD strength will ultimately be the more dominant driver and as argued above we are instead wary of potential downside to bulk commodity prices,” say BoFAML.

Forecasts for AUD/USD

Ultimately, the difference between CBA’s outlook and BoFAML’s is a matter of degree rather than direction.

Both forecasts the Aussie lower against the US Dollar, but CBA see the pair gradually falling over 2017 from 0.75 in Q1, to 0.74 in Q2, to 0.72 in Q3 and 0.71 in Q4.

In 2018 they see a more substantial fall to 0.69 as more of Trump's policies get implements and the repatriation flows really start kicking in.

BoFAML, meanwhile, see a more rapid fall to 0.70 in 2017.

Clearly, China is an accelerating or decelerating factor depending on its outcome.

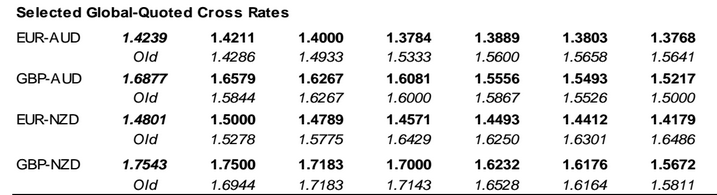

CBA's Forecasts for other AUD pairs – GBP/AUD and EUR/AUD

Commonwealth Bank has also published forecasts for other Aussie pairs.

They see the Pound falling quite substantially against the Aussie, with the pair at 1.6579 at the end of Q1 2017, 1.6278 at the end of Q2, 1.6081 at the end of Q3 and 1.5556 at the end of Q4.

EUR/AUD, meanwhile, is forecast to drop to a year low of 1.3784 in Q2 ( a big revision down from 1.5333 previously). It is forecast to end the year at 1.3803.