ECB Quantitative Easing + the Eurozone itself are Flawed Blast Deutsche Bank

Deutsche Bank have launched an extraordinary attack on the European Central Bank’s quantitative easing programme saying it lays the foundations for another crisis in the fundamentally unstable Eurozone.

The Group Chief Economist at Deutsche Bank has come out guns blazing against the European Central Bank’s asset purchase programme.

David Folkerts-Landau has accused the ECB of unwarranted self-praise over its huge monetary easing programme, in place since 2012.

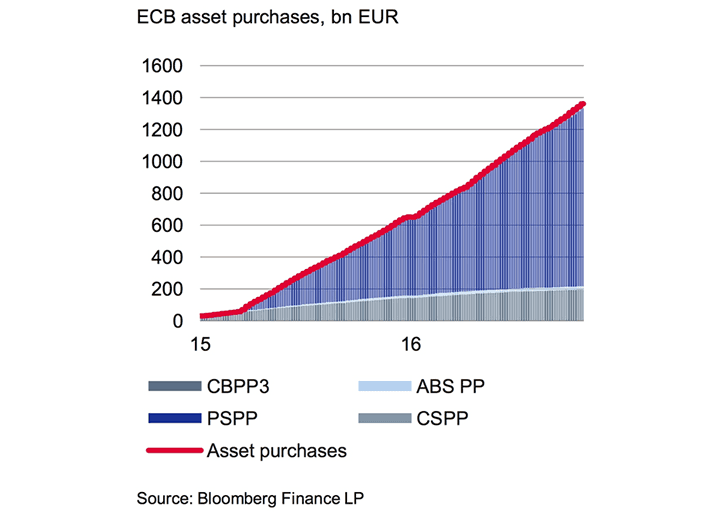

Monthly purchases in public and private sector securities now amount to €80 billion on average, from March 2015 until March 2016 this average monthly figure was €60 billion.

The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40%.

ECB President Mario Draghi has repeatedly said this programme is delivering economic growth and raising inflation levels, as intended.

“The reality is that since Mr Draghi’s infamous “whatever it takes” speech in 2012, the eurozone has delivered barely any growth, the worst labour market performance among industrial countries, unsustainable debt levels, and inflation far below the central bank’s own target,” says Folkerts-Landau.

“While the positive case for European Central Bank intervention is weak at best, it seems that the negative repercussions are becoming overwhelming,” adds the economist.

Furthermore, Folkerts-Landauhe says the Euro’s design is flawed:

“A combination of unified monetary policy and national fiscal policy where rules can be ignored without sanction – is flawed. But with Mr Draghi’s promise of “whatever it takes” the implied moral hazard was pushed into a much larger dimension.”

The accusations come as Deutsche Bank’s precarious financial position remains a focus for financial markets.

The share price remains within touching distance of historical lows and analysts point out that the negative impact to bank profitability stemming from ECB policy is one reason behind the weakness.

Low interest rate environments weigh on the margin of returns lenders can expect, therefore it would certainly be in Deutsche’s interests if the ECB were to start tapering its QE programme sooner than later.

Five Reasons why Quantitative Easing is Dangerous

Deutsche Bank make the following five arguments against the ECB’s policy stance:

1) A paradox of ECB intervention: That monetary policy stifled the very reform momentum it sought to create.

“Up until July 2012, high interest rates and refinancing threats forced governments to be serious about reforms. Indeed, pre-2012, more than half the growth initiatives recommended by the OECD were being implemented across the eurozone.

“But last year just twenty per cent were. ECB intervention has curtailed the prospect of significant reforms in labour markets, legal systems, welfare systems, and tax systems across the continent.”

2) Bond prices have lost their market-derived signalling function.

“Since investors began to anticipate sovereign purchases by the central bank in late 2014, intra-eurozone government bond spreads have been locked together. In turn, misrepresentative sovereign yields distort the whole fixed income universe that is priced off government debt.”

3) Increasing concentration of risk on the eurosystem balance sheet. This is expected to be EUR 2trn by March 2018.

“In the event of a debt restructuring of a eurozone member, the liabilities of the national central bank are likely to be borne by the taxpayers of the other eurozone member states, even if losses are spread over a long period. Fundamentally, however, the debt will have been socialised.”

4) ECB intervention has not been a net positive for eurozone savers.

“While high and stable revaluation gains have buttressed total returns over recent years, this is clearly a one-time gain. Today, rising energy prices, the shortage of high coupons and ultimately mean-reversion are likely to take their toll.”

5)Misallocation of capital caused by ECB policy is preventing creative

destruction and causing asset bubbles.

“Increased lending has gone mostly to low quality existing borrowers while obviating troubled banks from the need to write down loans. Without creative destruction in ailing industries, investors in high-saving countries have simply bid-up the price of healthy assets.”